EX-99.2

Published on November 4, 2025

| RENEWAL AND TRANSITION SUPPLEMENTAL OPERATING AND FINANCIAL DATA THIRD QUARTER 2025 |

| 3Q 2025 SUPPLEMENTAL REPORT INVESTMENTS 3 Portfolio Snapshot Acquisitions Mortgage Loans Joint Ventures Purchase Options PORTFOLIO 7 Proforma Activities Proforma Overview Proforma Diversification - Geography Proforma Seniors Housing Operating Portfolio ("SHOP") Diversification Proforma Real Estate Investments (Excluding SHOP) Diversification - Operators Proforma Real Estate Investments (Excluding SHOP) - Maturity Real Estate Investments (Excluding SHOP) - Metrics FINANCIAL 17 Enterprise Value Debt Metrics Proforma Debt Maturity Financial Data Summary Reconciliation of 2025 Guidance Consolidated Statements of Income Consolidated Balance Sheets Funds from Operations GLOSSARY 28 FORWARD-LOOKING STATEMENTS 30 AND NON-GAAP INFORMATION 2 LEADERSHIP Any opinions, estimates, or forecasts regarding LTC’s performance made by the analysts listed above do not represent the opinions, estimates, and forecasts of LTC or its management. BOARD OF DIRECTORS ANALYSTS LTC PROPERTIES, INC. 3011 Townsgate Road, Suite 220 Westlake Village, CA 91361 805-981-8655 www.LTCreit.com TRANSFER AGENT Broadridge Shareholder Services c/o Broadridge Corporate Issuer Solutions 1155 Long Island Avenue Edgewood, NY 11717-8309 ATTN: IWS 866-708-5586 WENDY SIMPSON Executive Chairman CORNELIA CHENG Sustainability and Corporate Responsibility Committee Chairman DAVID GRUBER Investment Committee Chairman JEFFREY HAWKEN Compensation Committee Chairman BRADLEY PREBER Audit Committee Chairman TIMOTHY TRICHE, MD Lead Independent Director and Nominating & Corporate Governance Committee Chairman JUAN SANABRIA BMO Capital Markets Corp. RICHARD ANDERSON Cantor Fitzgerald AARON HECHT Citizens JMP Securities, LLC OMOTAYO OKUSANYA Deutsche Bank Securities Inc. JOE DICKSTEIN Jefferies LLC AUSTIN WURSCHMIDT KeyBanc Capital Markets, Inc. MICHAEL CARROLL RBC Capital Markets Corp. JOHN KILICHOWSKI Wells Fargo Securities, LLC WENDY SIMPSON Executive Chairman PAM KESSLER Co-President and Co-CEO CLINT MALIN Co-President and Co-CEO CECE CHIKHALE EVP, Chief Financial Officer, Treasurer and Secretary DAVID BOITANO EVP, Chief Investment Officer GIBSON SATTERWHITE EVP, Asset Management MIKE BOWDEN SVP, Investments MANDI HOGAN SVP, Marketing TABLE OF CONTENTS CONTACT INFORMATION |

| 3Q 2025 SUPPLEMENTAL REPORT INVESTMENTS I 3 PORTFOLIO SNAPSHOT (AS OF NOVEMBER 4, 2025) OPERATORS 31 STATES 24 PROPERTIES 187 45.9% 20.0% 15.4% 16.8% 1.1% INVESTMENT TYPE 0.8% OWNED PORTFOLIO - NNN OWNED ACCOUNTED FOR AS FINANCING RECEIVABLES MORTGAGE LOANS NOTES RECEIVABLE UNCONSOLIDATED JOINT VENTURES OWNED PORTFOLIO - SHOP UNITS/BEDS 16,275 SENIORS HOUSING OPERATING PORTFOLIO (“SHOP”) 42.3% 20.0% 37.1% 0.6% PROPERTY TYPE SENIORS HOUSING - NNN SKILLED NURSING OTHER/UDP SENIORS HOUSING - SHOP ACQUISITIONS • $292 million • 9 properties • 4 operators new to LTC (Discovery, Charter, Lifespark and Arbor) PIPELINE • 4Q 2025 - Expect to close ≈$70 million in SHOP acquisitions over the next 60 days • 1Q 2026 - Expect to close an additional ≈$110 million in SHOP acquisitions in January SHOP SEGMENT • 22 Properties • 6 Operators • 1,665 units • Two NNN conversions and four acquisitions |

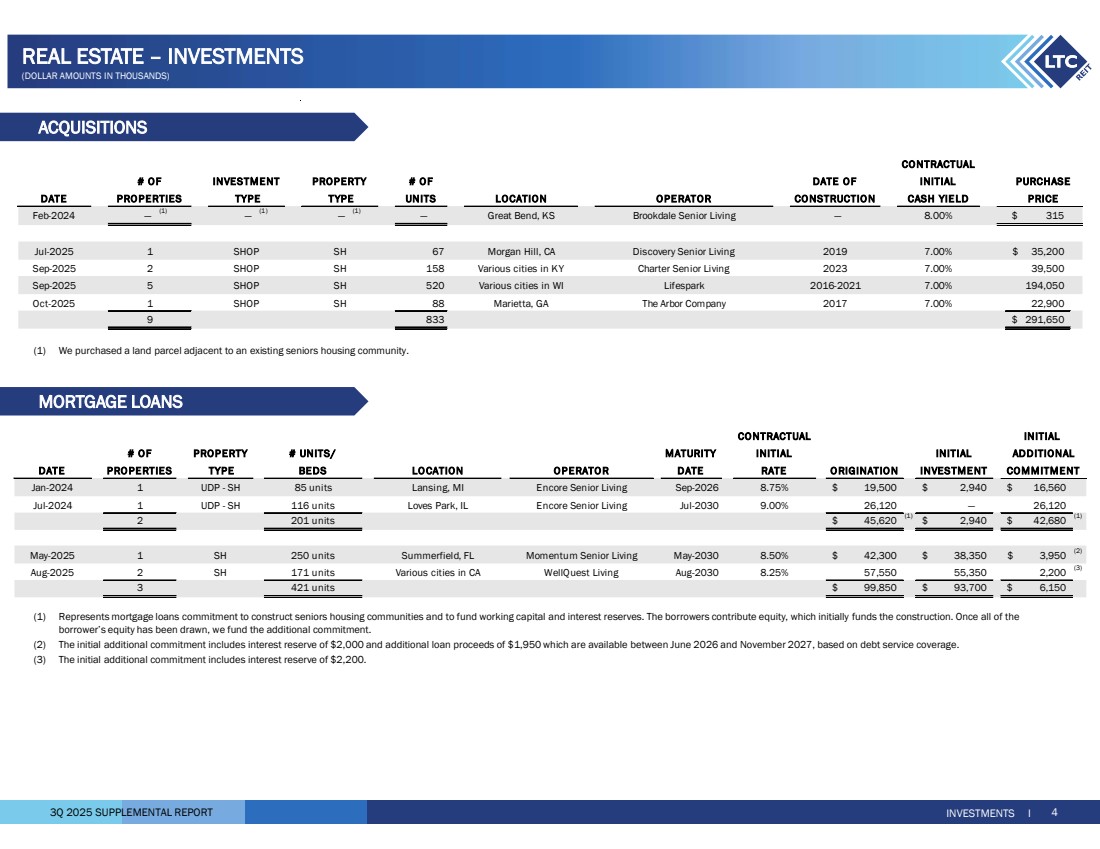

| 3Q 2025 SUPPLEMENTAL REPORT MORTGAGE LOANS INVESTMENTS I 4 (1) Represents mortgage loans commitment to construct seniors housing communities and to fund working capital and interest reserves. The borrowers contribute equity, which initially funds the construction. Once all of the borrower’s equity has been drawn, we fund the additional commitment. (2) The initial additional commitment includes interest reserve of $2,000 and additional loan proceeds of $1,950 which are available between June 2026 and November 2027, based on debt service coverage. (3) The initial additional commitment includes interest reserve of $2,200. REAL ESTATE – INVESTMENTS (DOLLAR AMOUNTS IN THOUSANDS) # OF PROPERTY # UNITS/ MATURITY INITIAL PRO PERTIES TYPE BEDS LO CATION OPERATO R DATE O RIGINATIO N INVESTME NT 1 UDP - SH 85 units Lansing, MI Encore Senior Living Sep-2026 8.75% 19,500 $ 2,940 $ 16,560 $ 1 UDP - SH 116 units Loves Park, IL Encore Senior Living Jul-2030 9.00% 26,120 — 26,120 2 201 units 45,620 $ (1) $ 42,680 2,940 $ (1) 1 SH 250 units Summerfield, FL Momentum Senior Living May-2030 8.50% 42,300 $ 38,350 $ 3,950 $ (2) 2 SH 171 units Various cities in CA WellQuest Living Aug-2030 8.25% 57,550 55,350 2,200 (3) 3 421 units 99,850 $ 93,700 $ 6,150 $ Aug-2025 CONTRACTUAL INITIAL Jan-2024 Jul-2024 COMMITMENT INITIAL ADDITIONAL RATE May-2025 DATE ACQUISITIONS CONTRACTUAL # OF INVESTMENT PROPERTY # OF DATE OF INITIAL PRO PERTIES TYPE TYPE UNITS LOCATION OPE RATOR CO NSTRUCTIO N CASH YIE LD — (1) — (1) — (1) — Great Bend, KS Brookdale Senior Living — 8.00% 315 $ 1 SHOP SH 67 Morgan Hill, CA Discovery Senior Living 2019 7.00% 35,200 $ 2 SHOP SH 158 Various cities in KY Charter Senior Living 2023 7.00% 39,500 5 SHOP SH 520 Various cities in WI Lifespark 2016-2021 7.00% 194,050 1 SHOP SH 88 Marietta, GA The Arbor Company 2017 7.00% 22,900 9 833 291,650 $ Jul-2025 Sep-2025 Oct-2025 Sep-2025 Feb-2024 DATE PURCHASE PRICE (1) We purchased a land parcel adjacent to an existing seniors housing community. |

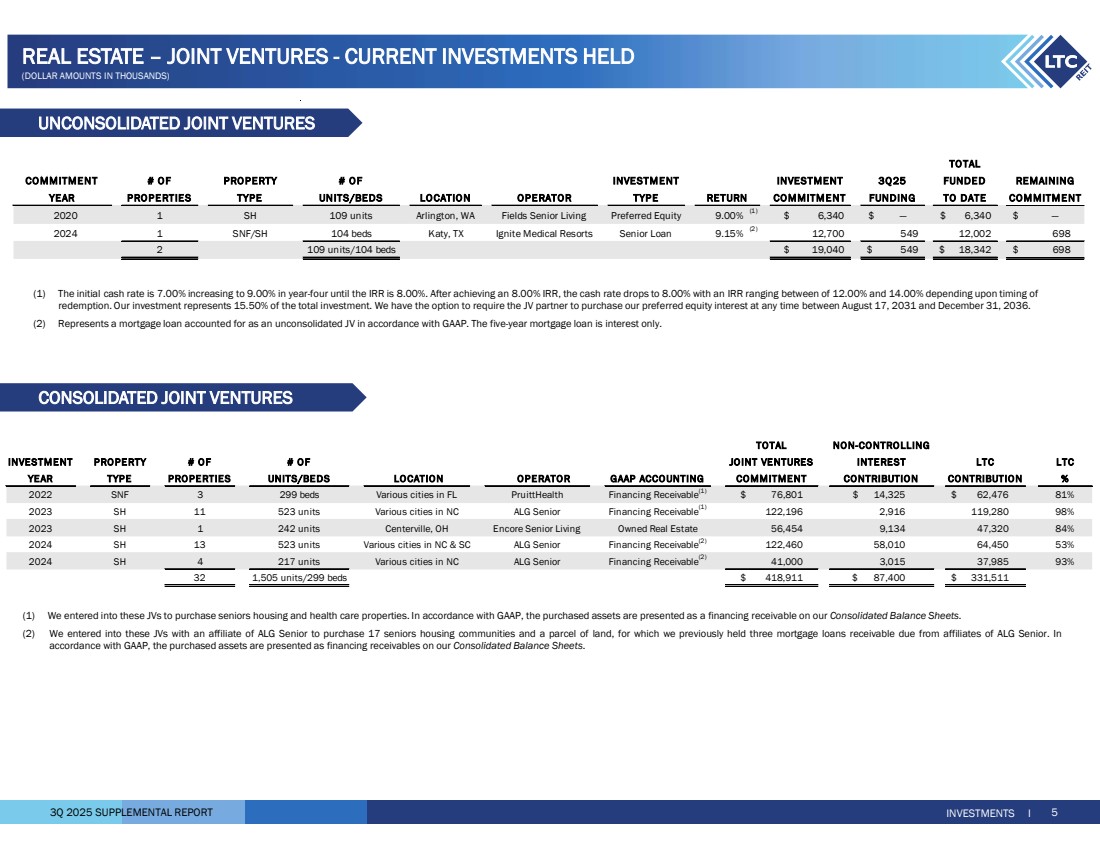

| 3Q 2025 SUPPLEMENTAL REPORT (1) The initial cash rate is 7.00% increasing to 9.00% in year-four until the IRR is 8.00%. After achieving an 8.00% IRR, the cash rate drops to 8.00% with an IRR ranging between of 12.00% and 14.00% depending upon timing of redemption. Our investment represents 15.50% of the total investment. We have the option to require the JV partner to purchase our preferred equity interest at any time between August 17, 2031 and December 31, 2036. (2) Represents a mortgage loan accounted for as an unconsolidated JV in accordance with GAAP. The five-year mortgage loan is interest only. CONSOLIDATED JOINT VENTURES UNCONSOLIDATED JOINT VENTURES INVESTMENTS I 5 (1) We entered into these JVs to purchase seniors housing and health care properties. In accordance with GAAP, the purchased assets are presented as a financing receivable on our Consolidated Balance Sheets. (2) We entered into these JVs with an affiliate of ALG Senior to purchase 17 seniors housing communities and a parcel of land, for which we previously held three mortgage loans receivable due from affiliates of ALG Senior. In accordance with GAAP, the purchased assets are presented as financing receivables on our Consolidated Balance Sheets. INVESTMENT PROPERTY # OF # OF LTC YEAR TYPE PROPERTIES UNITS/BEDS LOCATION OPERATOR GAAP ACCOUNTING % 2022 SNF 3 299 beds Various cities in FL PruittHealth Financing Receivable(1) $ 14,325 76,801 $ 62,476 $ 81% 2023 SH 11 523 units Various cities in NC ALG Senior Financing Receivable(1) 2,916 122,196 119,280 98% 2023 SH 1 242 units Centerville, OH Encore Senior Living Owned Real Estate 56,454 9,134 47,320 84% 2024 SH 13 523 units Various cities in NC & SC ALG Senior Financing Receivable(2) 58,010 122,460 64,450 53% 2024 SH 4 217 units Various cities in NC ALG Senior Financing Receivable(2) 3,015 41,000 37,985 93% 32 1,505 units/299 beds 418,911 $ 87,400 $ 331,511 $ TOTAL NON-CONTROLLING JOINT VENTURES INTEREST LTC COMMITMENT CONTRIBUTION CONTRIBUTION TO TAL # OF PROPERTY # OF INVESTMENT 3Q25 FUNDED PROPERTIES TYPE UNITS/BEDS LOCATION OPERATOR TYPE FUNDING TO DATE 2020 1 SH 109 units Arlington, WA Fields Senior Living Preferred Equity 9.00% (1) $ — 6,340 $ 6,340 $ — $ 2024 1 SNF/SH 104 beds Katy, TX Ignite Medical Resorts Senior Loan 9.15% (2) 549 12,700 12,002 698 2 109 units/104 beds 19,040 $ 549 $ 18,342 $ 698 $ COMMITMENT INVESTMENT COMMITMENT REMAINING YEAR COMMITMENT RETURN REAL ESTATE – JOINT VENTURES - CURRENT INVESTMENTS HELD (DOLLAR AMOUNTS IN THOUSANDS) |

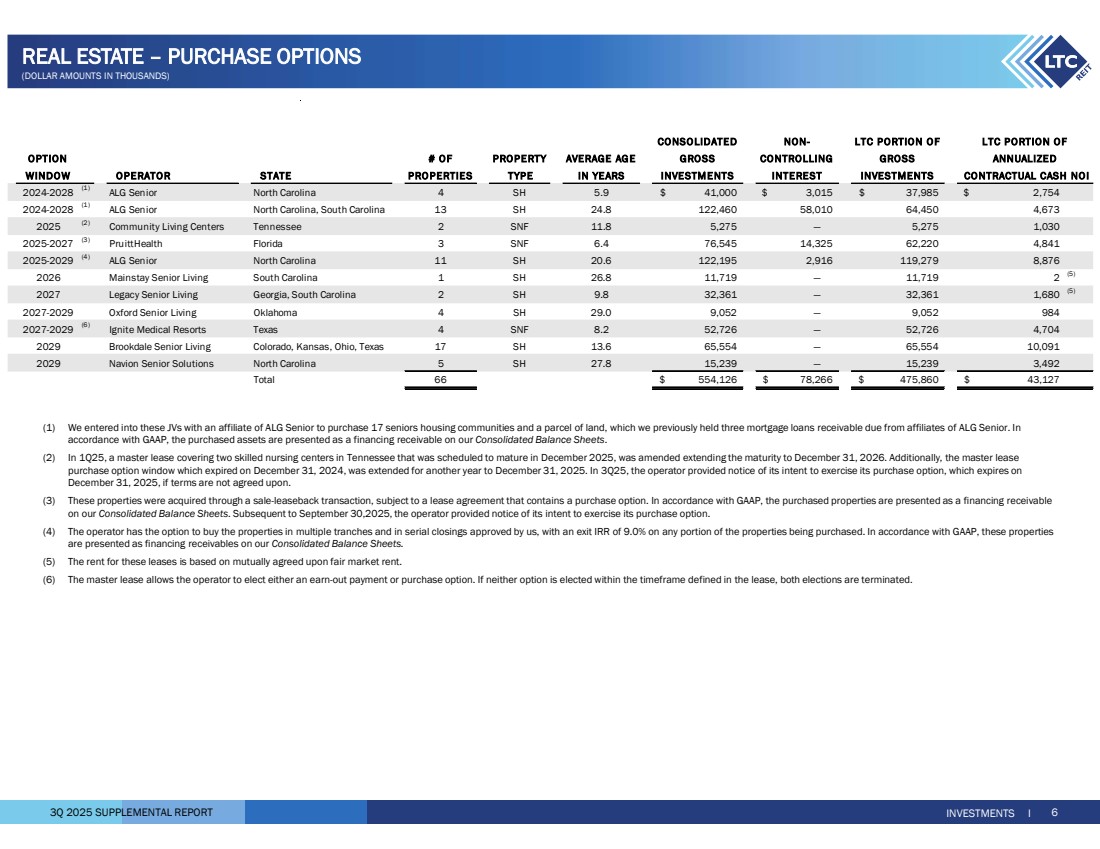

| 3Q 2025 SUPPLEMENTAL REPORT INVESTMENTS I 6 CONSOLIDATED NON-OPTION # OF PROPERTY AVERAGE AGE GROSS CONTROLLING GROSS WINDOW OPERATOR STATE PRO PERTIES TYPE IN YEARS INVESTMENTS INTEREST INVESTMENTS 2024-2028 (1) ALG Senior North Carolina 4 SH 5.9 41,000 $ 3,015 $ 37,985 $ 2,754 $ 2024-2028 (1) ALG Senior North Carolina, South Carolina 13 SH 24.8 122,460 58,010 64,450 4,673 2025 (2) Community Living Centers Tennessee 2 SNF 11.8 5,275 — 5,275 1,030 2025-2027 (3) PruittHealth Florida 3 SNF 6.4 76,545 14,325 62,220 4,841 2025-2029 (4) ALG Senior North Carolina 11 SH 20.6 122,195 2,916 119,279 8,876 2026 Mainstay Senior Living South Carolina 1 SH 26.8 11,719 — 11,719 2 (5) 2027 Legacy Senior Living Georgia, South Carolina 2 SH 9.8 32,361 — 32,361 1,680 (5) 2027-2029 Oxford Senior Living Oklahoma 4 SH 29.0 9,052 — 9,052 984 2027-2029 (6) Ignite Medical Resorts Texas 4 SNF 8.2 52,726 — 52,726 4,704 2029 Brookdale Senior Living Colorado, Kansas, Ohio, Texas 17 SH 13.6 65,554 — 65,554 10,091 2029 Navion Senior Solutions North Carolina 5 SH 27.8 15,239 — 15,239 3,492 Total 66 554,126 $ 78,266 $ 475,860 $ 43,127 $ ANNUALIZED CONTRACTUAL CASH NOI LTC PORTION OF LTC PORTION OF (1) We entered into these JVs with an affiliate of ALG Senior to purchase 17 seniors housing communities and a parcel of land, which we previously held three mortgage loans receivable due from affiliates of ALG Senior. In accordance with GAAP, the purchased assets are presented as a financing receivable on our Consolidated Balance Sheets. (2) In 1Q25, a master lease covering two skilled nursing centers in Tennessee that was scheduled to mature in December 2025, was amended extending the maturity to December 31, 2026. Additionally, the master lease purchase option window which expired on December 31, 2024, was extended for another year to December 31, 2025. In 3Q25, the operator provided notice of its intent to exercise its purchase option, which expires on December 31, 2025, if terms are not agreed upon. (3) These properties were acquired through a sale-leaseback transaction, subject to a lease agreement that contains a purchase option. In accordance with GAAP, the purchased properties are presented as a financing receivable on our Consolidated Balance Sheets. Subsequent to September 30,2025, the operator provided notice of its intent to exercise its purchase option. (4) The operator has the option to buy the properties in multiple tranches and in serial closings approved by us, with an exit IRR of 9.0% on any portion of the properties being purchased. In accordance with GAAP, these properties are presented as financing receivables on our Consolidated Balance Sheets. (5) The rent for these leases is based on mutually agreed upon fair market rent. (6) The master lease allows the operator to elect either an earn-out payment or purchase option. If neither option is elected within the timeframe defined in the lease, both elections are terminated. REAL ESTATE – PURCHASE OPTIONS (DOLLAR AMOUNTS IN THOUSANDS) |

| 3Q 2025 SUPPLEMENTAL REPORT PORTFOLIO I 7 Proforma represents amounts as of September 30, 2025 adjusted as follows: Annualized SHOP NOI at an estimated year-one yield of 7% for the $194,050 3Q25 acquisition of five seniors housing communities totaling 520 units in Wisconsin. We annualized interest expense for the borrowing under our unsecured revolving line of credit related to this portfolio acquisition. Annualized SHOP NOI at an estimated year-one yield of 7% for the $22,900 4Q25 acquisition of an 88-unit seniors housing community in Georgia. We annualized interest expense for the assumed borrowing under our unsecured revolving line of credit related to this acquisition. For further discussion see our Subsequent Events on page 14. Reduction in annualized interest expense for the assumed paydown under our unsecured revolving line of credit from $120,800 of proceeds received from the 4Q25 sale of a portfolio of seven skilled nursing centers. Further, we adjusted for the corresponding elimination of assets and rental income related to this portfolio. For further discussion see our Subsequent Events on page 14. Reduction in annualized interest expense for the 4Q25 paydown of $21,000 under our unsecured revolving line of credit from excess cash on hand at September 30, 2025 and proceeds from the sale of 281,400 shares of our common stock under our equity distribution agreement during 4Q25. PROFORMA ACTIVITIES (DOLLAR AMOUNTS IN THOUSANDS) |

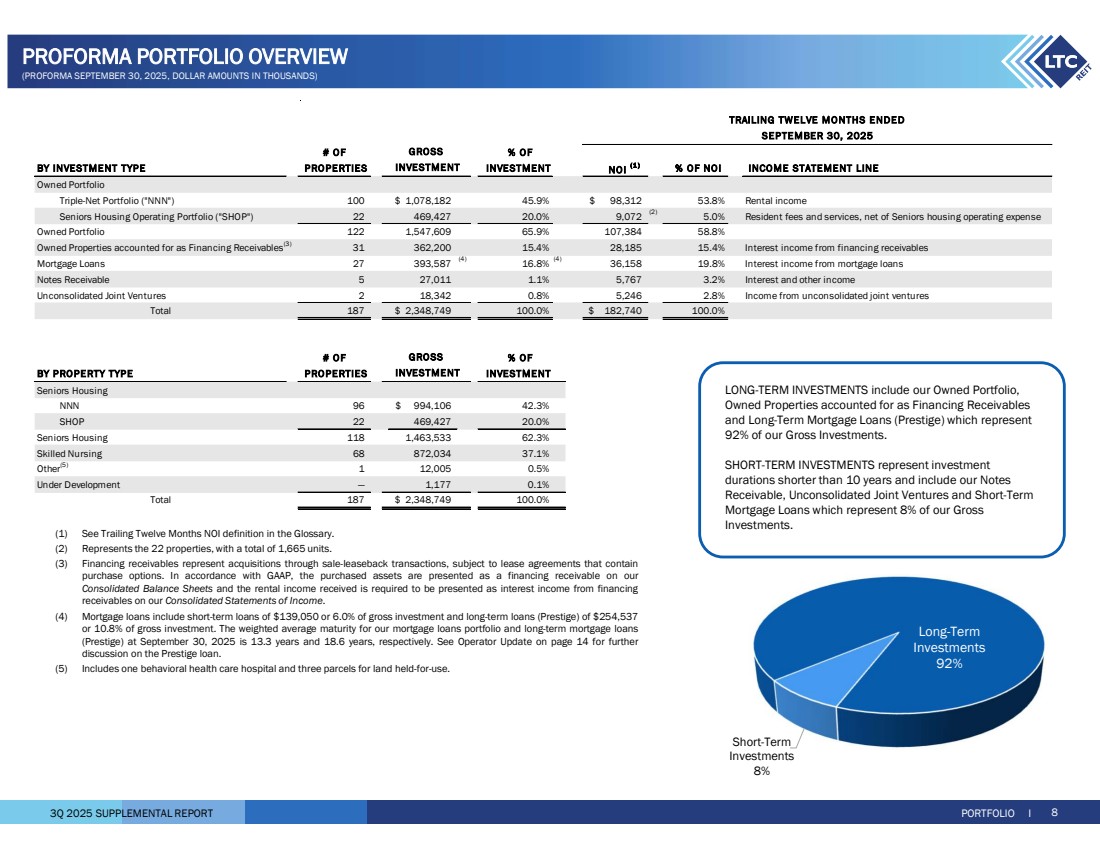

| 3Q 2025 SUPPLEMENTAL REPORT # OF % OF BY INVESTMENT TYPE PROPERTIES INVESTMENT NOI (1 ) % OF NOI INCOME STATEMENT LINE Owned Portfolio Triple-Net Portfolio ("NNN") 100 1,078,182 $ 45.9% 98,312 $ 53.8% Rental income Seniors Housing Operating Portfolio ("SHOP") 22 469,427 20.0% 9,072 (2) 5.0% Resident fees and services, net of Seniors housing operating expense Owned Portfolio 122 1,547,609 65.9% 107,384 58.8% Owned Properties accounted for as Financing Receivables(3) 362,200 31 15.4% 28,185 15.4% Interest income from financing receivables Mortgage Loans 27 393,587 (4) 16.8% (4) 19.8% Interest income from mortgage loans 36,158 Notes Receivable 5 27,011 1.1% 5,767 3.2% Interest and other income Unconsolidated Joint Ventures 2 18,342 0.8% 5,246 2.8% Income from unconsolidated joint ventures Total 187 2,348,749 $ 100.0% 182,740 $ 100.0% # OF % OF BY PROPERTY TYPE PROPERTIES INVESTMENT Seniors Housing NNN 96 994,106 $ 42.3% SHOP 22 469,427 20.0% Seniors Housing 118 1,463,533 62.3% Skilled Nursing 68 872,034 37.1% Other(5) 12,005 1 0.5% Under Development — 1,177 0.1% Total 187 2,348,749 $ 100.0% INVESTMENT GROSS INVESTMENT TRAILING TWELVE MONTHS ENDED SEPTEMBER 30, 2025 GROSS PORTFOLIO I (1) See Trailing Twelve Months NOI definition in the Glossary. (2) Represents the 22 properties, with a total of 1,665 units. (3) Financing receivables represent acquisitions through sale-leaseback transactions, subject to lease agreements that contain purchase options. In accordance with GAAP, the purchased assets are presented as a financing receivable on our Consolidated Balance Sheets and the rental income received is required to be presented as interest income from financing receivables on our Consolidated Statements of Income. (4) Mortgage loans include short-term loans of $139,050 or 6.0% of gross investment and long-term loans (Prestige) of $254,537 or 10.8% of gross investment. The weighted average maturity for our mortgage loans portfolio and long-term mortgage loans (Prestige) at September 30, 2025 is 13.3 years and 18.6 years, respectively. See Operator Update on page 14 for further discussion on the Prestige loan. (5) Includes one behavioral health care hospital and three parcels for land held-for-use. 8 LONG-TERM INVESTMENTS include our Owned Portfolio, Owned Properties accounted for as Financing Receivables and Long-Term Mortgage Loans (Prestige) which represent 92% of our Gross Investments. SHORT-TERM INVESTMENTS represent investment durations shorter than 10 years and include our Notes Receivable, Unconsolidated Joint Ventures and Short-Term Mortgage Loans which represent 8% of our Gross Investments. Long-Term Investments 92% Short-Term Investments 8% PROFORMA PORTFOLIO OVERVIEW (PROFORMA SEPTEMBER 30, 2025, DOLLAR AMOUNTS IN THOUSANDS) |

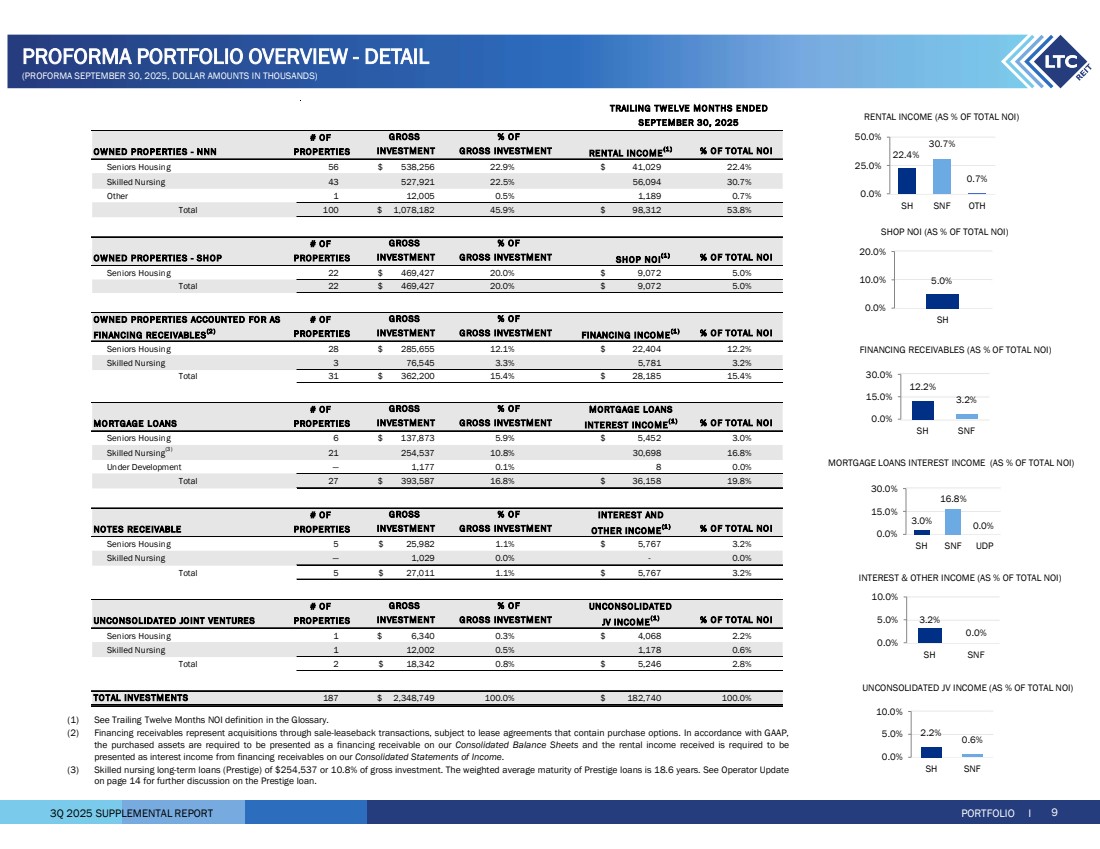

| 3Q 2025 SUPPLEMENTAL REPORT PORTFOLIO I 9 # OF OWNED PRO PERTIES - NNN PROPERTIES RENTAL INCOME(1 ) Seniors Housing 56 538,256 $ 22.9% 41,029 $ 22.4% Skilled Nursing 43 527,921 22.5% 56,094 30.7% Other 1 12,005 0.5% 1,189 0.7% Total 100 1,078,182 $ 45.9% 98,312 $ 53.8% # OF OWNED PRO PERTIES - SHOP PROPERTIES SHOP NOI(1 ) Seniors Housing 22 469,427 $ 20.0% 9,072 $ 5.0% Total 22 469,427 $ 20.0% 9,072 $ 5.0% OWNED PRO PERTIES ACCOUNTED FO R AS # OF FINANCING RECEIVABLES(2 ) PROPERTIES FINANCING INCOME(1 ) Seniors Housing 28 285,655 $ 12.1% 22,404 $ 12.2% Skilled Nursing 3 76,545 3.3% 5,781 3.2% Total 31 362,200 $ 15.4% 28,185 $ 15.4% # OF MORTGAGE LOANS MO RTGAGE LOANS PROPERTIES INTEREST INCO ME(1 ) Seniors Housing 6 137,873 $ 5.9% 5,452 $ 3.0% Skilled Nursing(3) 254,537 21 10.8% 30,698 16.8% Under Development — 1,177 0.1% 8 0.0% Total 27 393,587 $ 16.8% 36,158 $ 19.8% # OF INTEREST AND NO TES RECEIVABLE PROPERTIES OTHER INCOME(1 ) Seniors Housing 5 25,982 $ 1.1% 5,767 $ 3.2% Skilled Nursing — 1,029 0.0% - 0.0% Total 5 27,011 $ 1.1% 5,767 $ 3.2% # OF UNCONSOLIDATED UNCONSOLIDATED JO INT VENTURES PROPERTIES JV INCO ME(1 ) Seniors Housing 1 6,340 $ 0.3% 4,068 $ 2.2% Skilled Nursing 1 12,002 0.5% 1,178 0.6% Total 2 18,342 $ 0.8% 5,246 $ 2.8% TO TAL INVESTMENTS 2,348,749 187 $ 100.0% 182,740 $ 100.0% GROSS INVESTMENT % O F GROSS INVESTMENT % O F TOTAL NO I % O F TOTAL NO I % O F TOTAL NO I INVESTMENT TRAILING TWELVE MO NTHS ENDED SEPTEMBER 30, 2025 GROSS % O F GROSS INVESTMENT % O F TOTAL NO I GROSS % O F INVESTMENT GROSS INVESTMENT % O F TOTAL NO I INVESTMENT GROSS GROSS INVESTMENT GROSS INVESTMENT % O F GROSS INVESTMENT % O F GROSS % O F INVESTMENT GROSS INVESTMENT % O F TOTAL NO I 22.4% 30.7% 0.7% 0.0% 25.0% 50.0% SH SNF OTH RENTAL INCOME (AS % OF TOTAL NOI) MORTGAGE LOANS INTEREST INCOME (AS % OF TOTAL NOI) INTEREST & OTHER INCOME (AS % OF TOTAL NOI) UNCONSOLIDATED JV INCOME (AS % OF TOTAL NOI) 3.0% 16.8% 0.0% 0.0% 15.0% 30.0% SH SNF UDP 3.2% 0.0% 0.0% 5.0% 10.0% SH SNF 2.2% 0.6% 0.0% 5.0% 10.0% SH SNF 12.2% 3.2% 0.0% 15.0% 30.0% SH SNF FINANCING RECEIVABLES (AS % OF TOTAL NOI) (1) See Trailing Twelve Months NOI definition in the Glossary. (2) Financing receivables represent acquisitions through sale-leaseback transactions, subject to lease agreements that contain purchase options. In accordance with GAAP, the purchased assets are required to be presented as a financing receivable on our Consolidated Balance Sheets and the rental income received is required to be presented as interest income from financing receivables on our Consolidated Statements of Income. (3) Skilled nursing long-term loans (Prestige) of $254,537 or 10.8% of gross investment. The weighted average maturity of Prestige loans is 18.6 years. See Operator Update on page 14 for further discussion on the Prestige loan. 5.0% 0.0% 10.0% 20.0% SH SHOP NOI (AS % OF TOTAL NOI) PROFORMA PORTFOLIO OVERVIEW - DETAIL (PROFORMA SEPTEMBER 30, 2025, DOLLAR AMOUNTS IN THOUSANDS) |

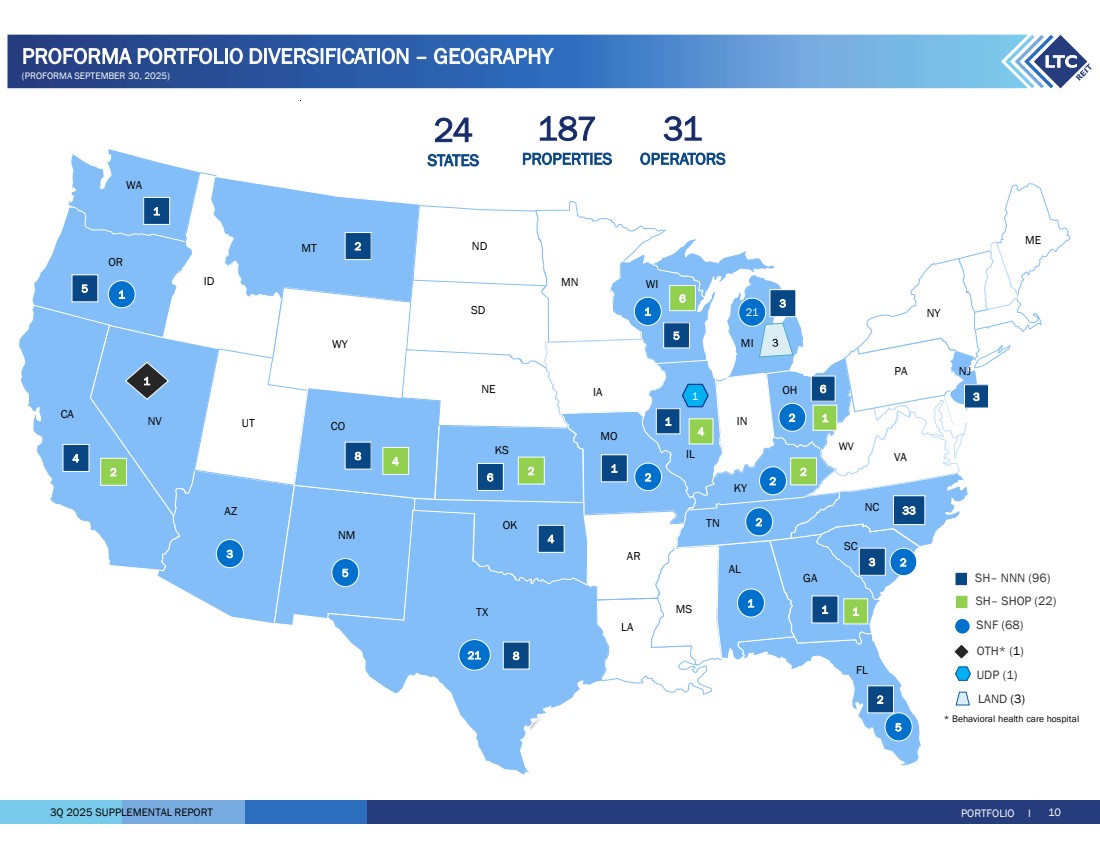

| 3Q 2025 SUPPLEMENTAL REPORT PORTFOLIO I 10 * Behavioral health care hospital SNF (68) SH– NNN (96) OTH* (1) LAND (3) UDP (1) CA WA ME NV WY IL AR WV ND NY OR AZ NM TX UT ID MT SD NE KS OK MS MN WI FL AL GA SC TN MO IA IN OH PA NJ NC VA CO KY 5 21 1 3 1 2 2 1 4 4 8 33 2 6 6 8 5 3 21 2 1 5 1 1 2 5 LA 1 2 3 MI 2 1 1 3 SH– SHOP (22) 4 2 2 4 6 1 24 STATES 187 PROPERTIES 31 OPERATORS 2 1 PROFORMA PORTFOLIO DIVERSIFICATION – GEOGRAPHY (PROFORMA SEPTEMBER 30, 2025) |

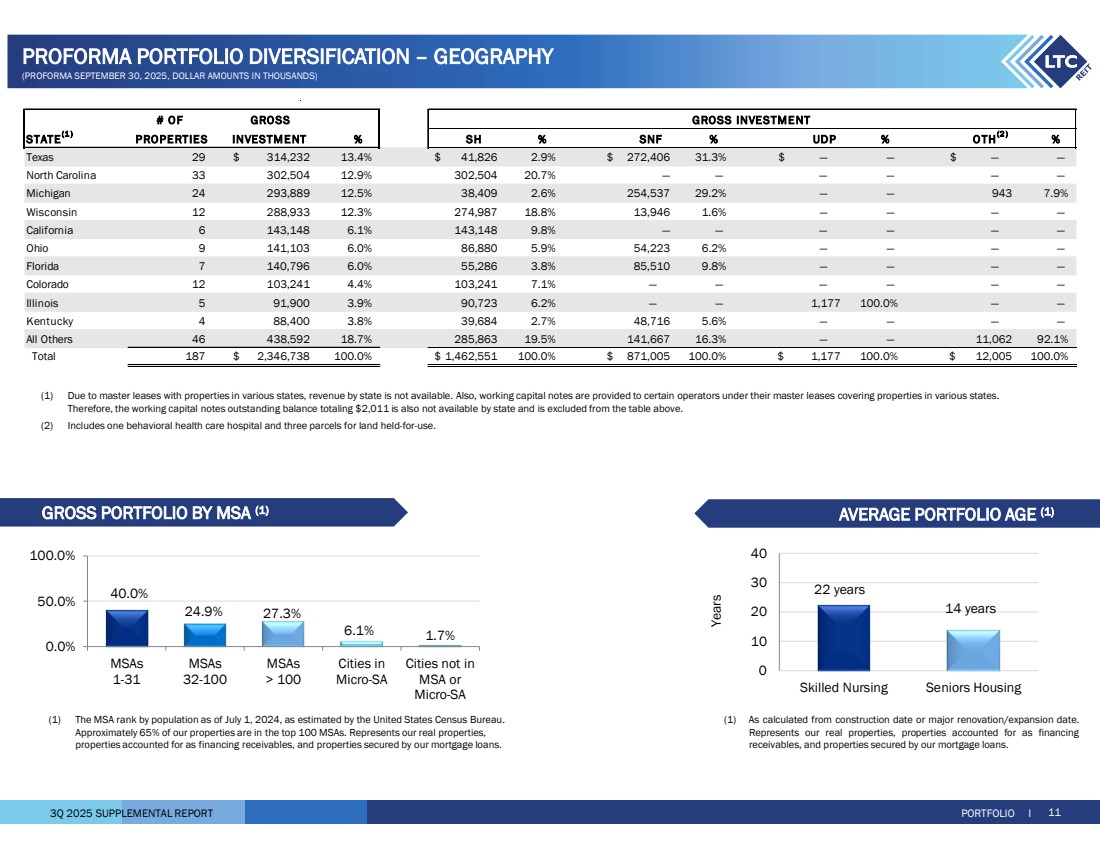

| 3Q 2025 SUPPLEMENTAL REPORT 40.0% 24.9% 27.3% 6.1% 1.7% 0.0% 50.0% 100.0% MSAs 1-31 MSAs 32-100 MSAs > 100 Cities in Micro-SA Cities not in MSA or Micro-SA 22 years 14 years 0 10 20 30 40 Skilled Nursing Seniors Housing Years (1) The MSA rank by population as of July 1, 2024, as estimated by the United States Census Bureau. Approximately 65% of our properties are in the top 100 MSAs. Represents our real properties, properties accounted for as financing receivables, and properties secured by our mortgage loans. (1) As calculated from construction date or major renovation/expansion date. Represents our real properties, properties accounted for as financing receivables, and properties secured by our mortgage loans. GROSS PORTFOLIO BY MSA (1) AVERAGE PORTFOLIO AGE (1) PORTFOLIO I 11 (1) Due to master leases with properties in various states, revenue by state is not available. Also, working capital notes are provided to certain operators under their master leases covering properties in various states. Therefore, the working capital notes outstanding balance totaling $2,011 is also not available by state and is excluded from the table above. (2) Includes one behavioral health care hospital and three parcels for land held-for-use. # OF STATE(1 ) PROPERTIES % SH % SNF % UDP % % Texas 29 314,232 $ 13.4% 41,826 $ 2.9% 272,406 $ 31.3% — $ — — $ — North Carolina 33 302,504 12.9% 302,504 20.7% — — — — — — Michigan 24 293,889 12.5% 38,409 2.6% 254,537 29.2% — — 943 7.9% Wisconsin 12 288,933 12.3% 274,987 18.8% 13,946 1.6% — — — — California 6 143,148 6.1% 143,148 9.8% — — — — — — Ohio 9 141,103 6.0% 86,880 5.9% 54,223 6.2% — — — — Florida 7 140,796 6.0% 55,286 3.8% 85,510 9.8% — — — — Colorado 12 103,241 4.4% 103,241 7.1% — — — — — — Illinois 5 91,900 3.9% 90,723 6.2% — — 1,177 100.0% — — Kentucky 4 88,400 3.8% 39,684 2.7% 48,716 5.6% — — — — All Others 46 438,592 18.7% 285,863 19.5% 141,667 16.3% — — 11,062 92.1% Total 187 2,346,738 $ 100.0% 1,462,551 $ 100.0% 871,005 $ 100.0% 1,177 $ 100.0% 12,005 $ 100.0% O TH(2 ) INVESTMENT GROSS GROSS INVESTMENT PROFORMA PORTFOLIO DIVERSIFICATION – GEOGRAPHY (PROFORMA SEPTEMBER 30, 2025, DOLLAR AMOUNTS IN THOUSANDS) |

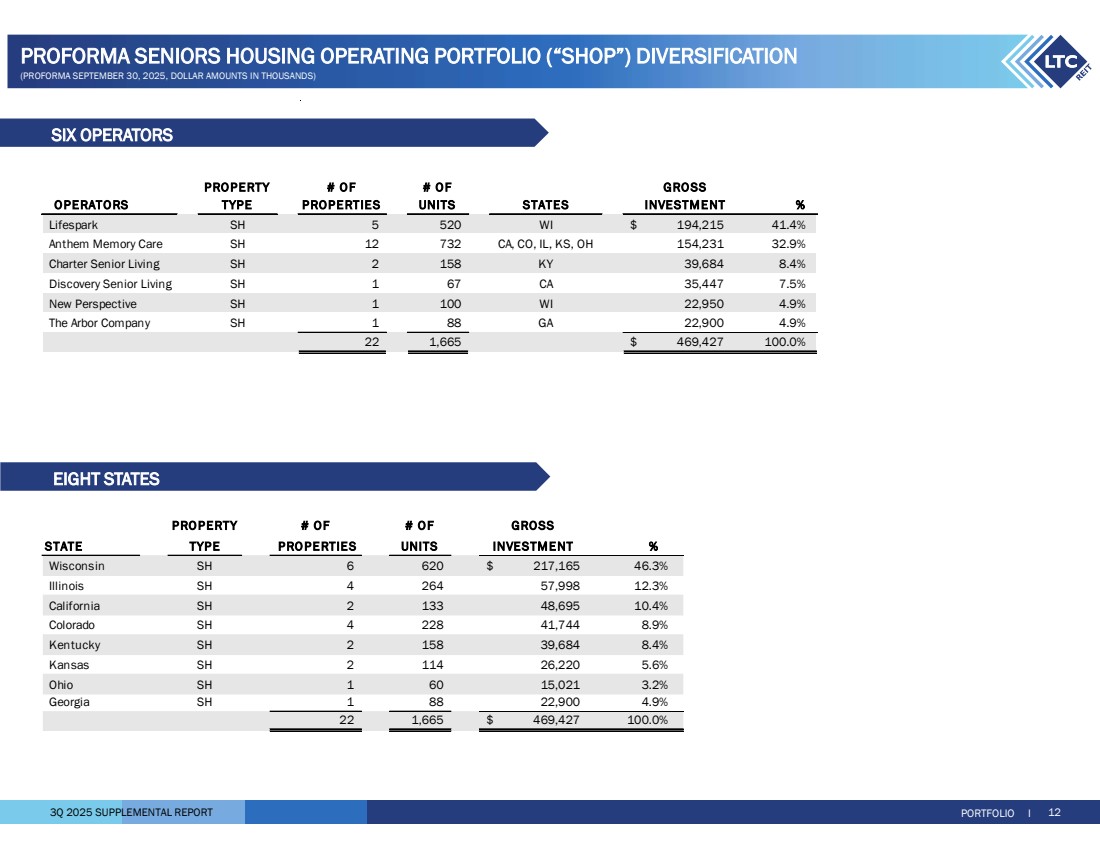

| 3Q 2025 SUPPLEMENTAL REPORT PORTFOLIO I 12 PROFORMA SENIORS HOUSING OPERATING PORTFOLIO (“SHOP”) DIVERSIFICATION (PROFORMA SEPTEMBER 30, 2025, DOLLAR AMOUNTS IN THOUSANDS) SIX OPERATORS EIGHT STATES PROPERTY # OF # OF GROSS STATE TYPE PRO PERTIES UNITS INVESTMENT % Wisconsin SH 6 620 217,165 $ 46.3% Illinois SH 4 264 57,998 12.3% California SH 2 133 48,695 10.4% Colorado SH 4 228 41,744 8.9% Kentucky SH 2 158 39,684 8.4% Kansas SH 2 114 26,220 5.6% Ohio SH 1 60 15,021 3.2% Georgia SH 1 88 22,900 4.9% 1,665 22 469,427 $ 100.0% PROPERTY # OF # OF GRO SS OPERATORS TYPE PROPERTIES UNITS STATES INVESTMENT % Lifespark SH 5 520 WI 194,215 $ 41.4% Anthem Memory Care SH 12 732 CA, CO, IL, KS, OH 154,231 32.9% Charter Senior Living SH 2 158 KY 39,684 8.4% Discovery Senior Living SH 1 67 CA 35,447 7.5% New Perspective SH 1 100 WI 22,950 4.9% The Arbor Company SH 1 88 GA 22,900 4.9% 1,665 22 469,427 $ 100.0% |

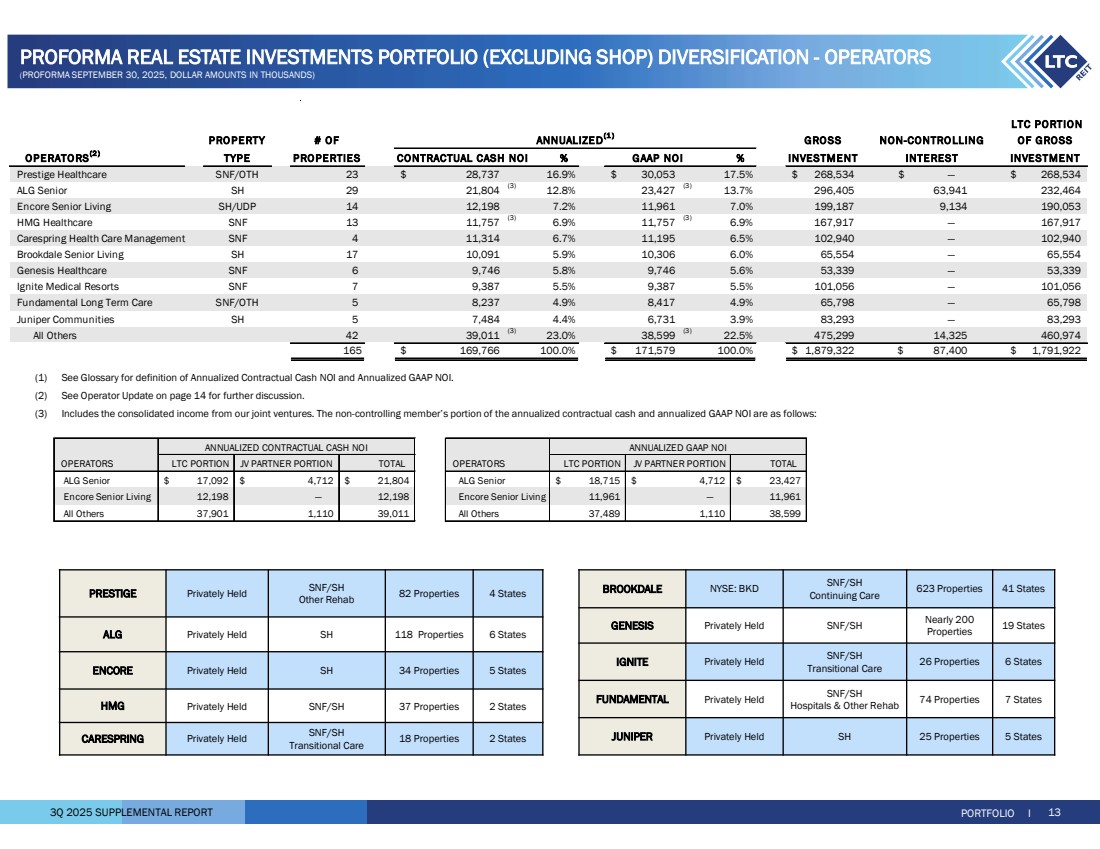

| 3Q 2025 SUPPLEMENTAL REPORT LTC PORTION PRO PERTY # OF GRO SS OF GROSS OPERATO RS(2 ) TYPE PROPERTIES CONTRACTUAL CASH NOI % % INVESTMENT INVESTMENT Prestige Healthcare SNF/OTH 23 28,737 $ 16.9% 30,053 $ 17.5% 268,534 $ — $ 268,534 $ ALG Senior SH 29 21,804 (3) 12.8% 23,427 (3) 13.7% 296,405 63,941 232,464 Encore Senior Living SH/UDP 14 12,198 7.2% 11,961 7.0% 199,187 9,134 190,053 HMG Healthcare SNF 13 11,757 (3) 6.9% 11,757 (3) 6.9% 167,917 — 167,917 Carespring Health Care Management SNF 4 11,314 6.7% 11,195 6.5% 102,940 — 102,940 Brookdale Senior Living SH 17 10,091 5.9% 10,306 6.0% 65,554 — 65,554 Genesis Healthcare SNF 6 9,746 5.8% 9,746 5.6% 53,339 — 53,339 Ignite Medical Resorts SNF 7 9,387 5.5% 9,387 5.5% 101,056 — 101,056 Fundamental Long Term Care SNF/OTH 5 8,237 4.9% 8,417 4.9% 65,798 — 65,798 Juniper Communities SH 5 7,484 4.4% 6,731 3.9% 83,293 — 83,293 All Others 42 39,011 (3) 23.0% 38,599 (3) 22.5% 475,299 14,325 460,974 165 169,766 $ 100.0% 171,579 $ 100.0% 1,879,322 $ 87,400 $ 1,791,922 $ GAAP NOI ANNUALIZED(1 ) NON-CONTRO LLING INTEREST PORTFOLIO I 13 PROFORMA REAL ESTATE INVESTMENTS PORTFOLIO (EXCLUDING SHOP) DIVERSIFICATION - OPERATORS (PROFORMA SEPTEMBER 30, 2025, DOLLAR AMOUNTS IN THOUSANDS) 623 Properties 41 States SNF/SH Continuing Care BROOKDALE NYSE: BKD 19 States Nearly 200 Properties GENESIS Privately Held SNF/SH 26 Properties 6 States SNF/SH Transitional Care IGNITE Privately Held 74 Properties 7 States SNF/SH Hospitals & Other Rehab FUNDAMENTAL Privately Held JUNIPER Privately Held SH 25 Properties 5 States 82 Properties 4 States SNF/SH Other Rehab PRESTIGE Privately Held ALG Privately Held SH 118 Properties 6 States ENCORE Privately Held SH 34 Properties 5 States HMG Privately Held SNF/SH 37 Properties 2 States 18 Properties 2 States SNF/SH Transitional Care CARESPRING Privately Held (1) See Glossary for definition of Annualized Contractual Cash NOI and Annualized GAAP NOI. (2) See Operator Update on page 14 for further discussion. (3) Includes the consolidated income from our joint ventures. The non-controlling member’s portion of the annualized contractual cash and annualized GAAP NOI are as follows: OPERATORS LTC PORTION JV PARTNER PORTION TOTAL OPERATORS LTC PORTION JV PARTNER PORTION TOTAL ALG Senior 17,092 $ 4,712 $ 21,804 $ ALG Senior 18,715 $ 4,712 $ 23,427 $ Encore Senior Living 12,198 — 12,198 Encore Senior Living 11,961 — 11,961 All Others 37,901 1,110 39,011 All Others 37,489 1,110 38,599 ANNUALIZED CONTRACTUAL CASH NOI ANNUALIZED GAAP NOI |

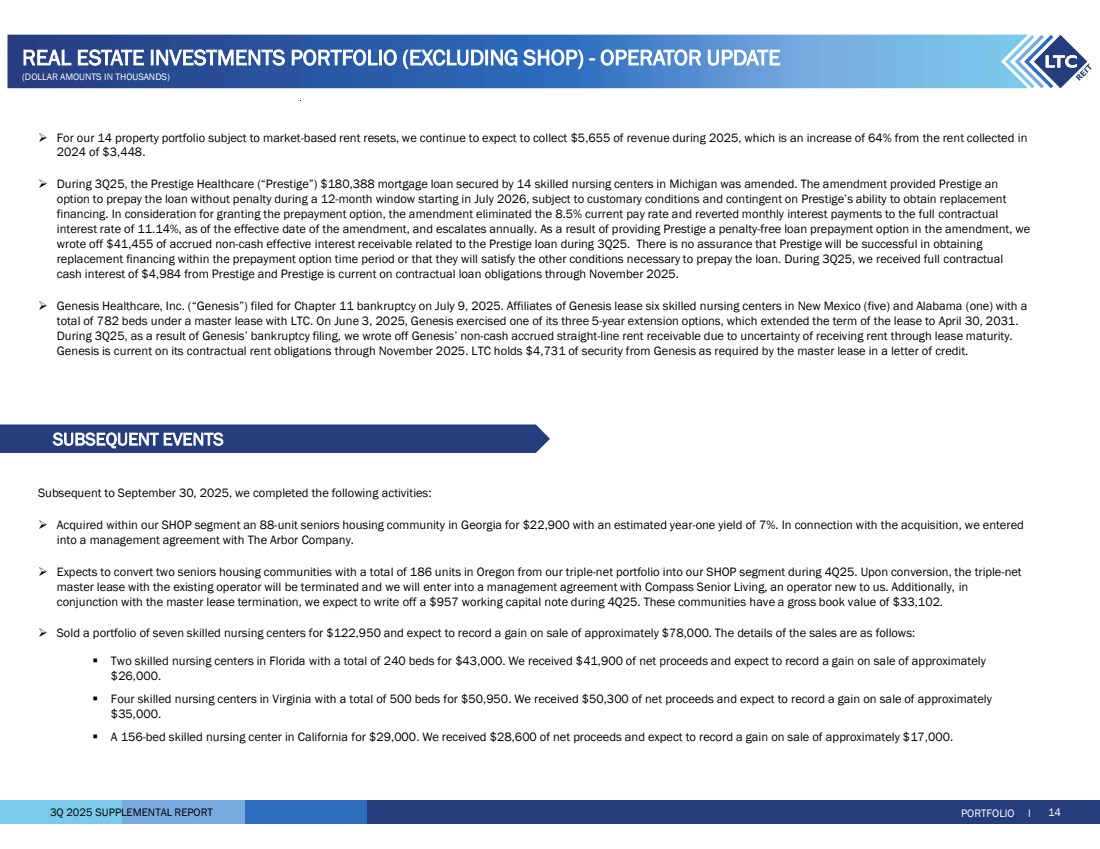

| 3Q 2025 SUPPLEMENTAL REPORT PORTFOLIO I 14 REAL ESTATE INVESTMENTS PORTFOLIO (EXCLUDING SHOP) - OPERATOR UPDATE (DOLLAR AMOUNTS IN THOUSANDS) For our 14 property portfolio subject to market-based rent resets, we continue to expect to collect $5,655 of revenue during 2025, which is an increase of 64% from the rent collected in 2024 of $3,448. During 3Q25, the Prestige Healthcare (“Prestige”) $180,388 mortgage loan secured by 14 skilled nursing centers in Michigan was amended. The amendment provided Prestige an option to prepay the loan without penalty during a 12-month window starting in July 2026, subject to customary conditions and contingent on Prestige’s ability to obtain replacement financing. In consideration for granting the prepayment option, the amendment eliminated the 8.5% current pay rate and reverted monthly interest payments to the full contractual interest rate of 11.14%, as of the effective date of the amendment, and escalates annually. As a result of providing Prestige a penalty-free loan prepayment option in the amendment, we wrote off $41,455 of accrued non-cash effective interest receivable related to the Prestige loan during 3Q25. There is no assurance that Prestige will be successful in obtaining replacement financing within the prepayment option time period or that they will satisfy the other conditions necessary to prepay the loan. During 3Q25, we received full contractual cash interest of $4,984 from Prestige and Prestige is current on contractual loan obligations through November 2025. Genesis Healthcare, Inc. (“Genesis”) filed for Chapter 11 bankruptcy on July 9, 2025. Affiliates of Genesis lease six skilled nursing centers in New Mexico (five) and Alabama (one) with a total of 782 beds under a master lease with LTC. On June 3, 2025, Genesis exercised one of its three 5-year extension options, which extended the term of the lease to April 30, 2031. During 3Q25, as a result of Genesis’ bankruptcy filing, we wrote off Genesis’ non-cash accrued straight-line rent receivable due to uncertainty of receiving rent through lease maturity. Genesis is current on its contractual rent obligations through November 2025. LTC holds $4,731 of security from Genesis as required by the master lease in a letter of credit. SUBSEQUENT EVENTS Subsequent to September 30, 2025, we completed the following activities: Acquired within our SHOP segment an 88-unit seniors housing community in Georgia for $22,900 with an estimated year-one yield of 7%. In connection with the acquisition, we entered into a management agreement with The Arbor Company. Expects to convert two seniors housing communities with a total of 186 units in Oregon from our triple-net portfolio into our SHOP segment during 4Q25. Upon conversion, the triple-net master lease with the existing operator will be terminated and we will enter into a management agreement with Compass Senior Living, an operator new to us. Additionally, in conjunction with the master lease termination, we expect to write off a $957 working capital note during 4Q25. These communities have a gross book value of $33,102. Sold a portfolio of seven skilled nursing centers for $122,950 and expect to record a gain on sale of approximately $78,000. The details of the sales are as follows: Two skilled nursing centers in Florida with a total of 240 beds for $43,000. We received $41,900 of net proceeds and expect to record a gain on sale of approximately $26,000. Four skilled nursing centers in Virginia with a total of 500 beds for $50,950. We received $50,300 of net proceeds and expect to record a gain on sale of approximately $35,000. A 156-bed skilled nursing center in California for $29,000. We received $28,600 of net proceeds and expect to record a gain on sale of approximately $17,000. |

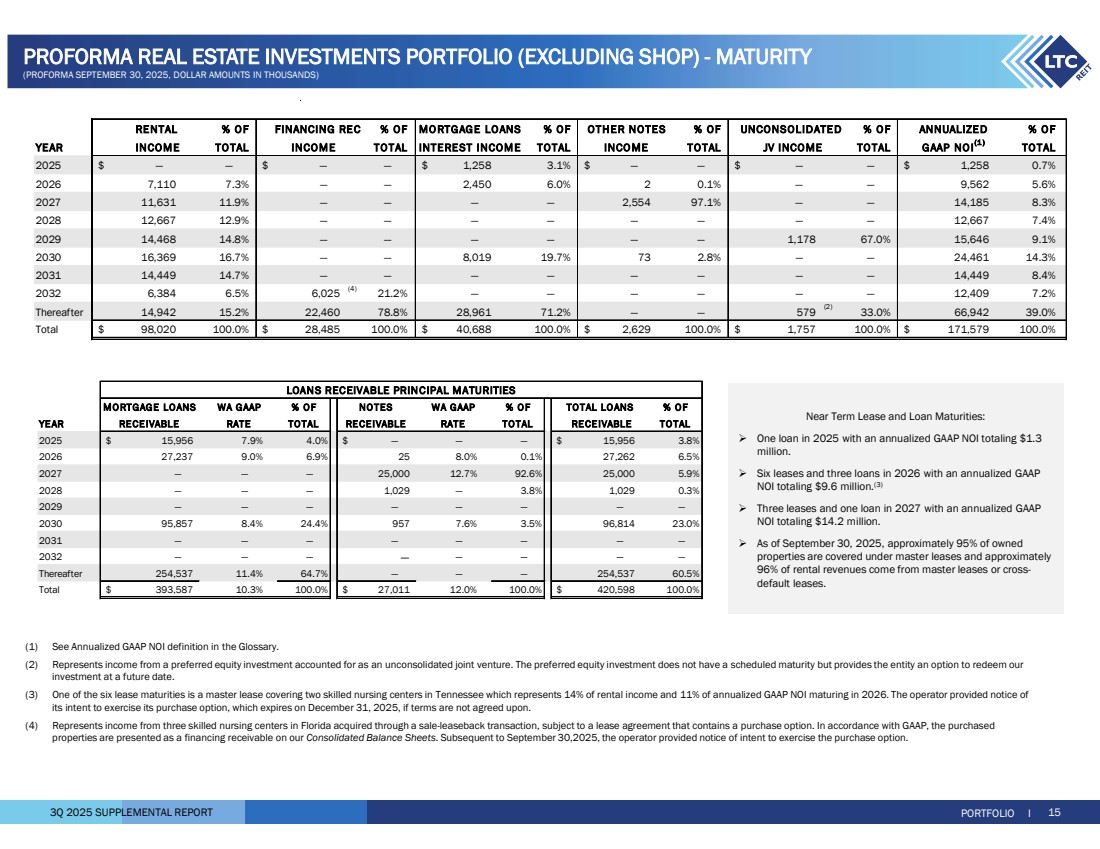

| 3Q 2025 SUPPLEMENTAL REPORT PROFORMA REAL ESTATE INVESTMENTS PORTFOLIO (EXCLUDING SHOP) - MATURITY (PROFORMA SEPTEMBER 30, 2025, DOLLAR AMOUNTS IN THOUSANDS) PORTFOLIO I 15 (1) See Annualized GAAP NOI definition in the Glossary. (2) Represents income from a preferred equity investment accounted for as an unconsolidated joint venture. The preferred equity investment does not have a scheduled maturity but provides the entity an option to redeem our investment at a future date. (3) One of the six lease maturities is a master lease covering two skilled nursing centers in Tennessee which represents 14% of rental income and 11% of annualized GAAP NOI maturing in 2026. The operator provided notice of its intent to exercise its purchase option, which expires on December 31, 2025, if terms are not agreed upon. (4) Represents income from three skilled nursing centers in Florida acquired through a sale-leaseback transaction, subject to a lease agreement that contains a purchase option. In accordance with GAAP, the purchased properties are presented as a financing receivable on our Consolidated Balance Sheets. Subsequent to September 30,2025, the operator provided notice of intent to exercise the purchase option. Near Term Lease and Loan Maturities: One loan in 2025 with an annualized GAAP NOI totaling $1.3 million. Six leases and three loans in 2026 with an annualized GAAP NOI totaling $9.6 million.(3) Three leases and one loan in 2027 with an annualized GAAP NOI totaling $14.2 million. As of September 30, 2025, approximately 95% of owned properties are covered under master leases and approximately 96% of rental revenues come from master leases or cross-default leases. % OF % OF % OF % OF % O F % O F YEAR TO TAL TOTAL TOTAL TOTAL TO TAL TO TAL 2025 — $ — — $ — 1,258 $ 3.1% — $ — — $ — 1,258 $ 0.7% 2026 7,110 7.3% — — 2,450 6.0% 2 0.1% — — 9,562 5.6% 2027 11,631 11.9% — — — — 2,554 97.1% — — 14,185 8.3% 2028 12,667 12.9% — — — — — — — — 12,667 7.4% 2029 14,468 14.8% — — — — — — 1,178 67.0% 15,646 9.1% 2030 16,369 16.7% — — 8,019 19.7% 73 2.8% — — 24,461 14.3% 2031 14,449 14.7% — — — — — — — — 14,449 8.4% 2032 6,384 6.5% 6,025 (4) 21.2% — — — — — — 12,409 7.2% Thereafter 14,942 15.2% 22,460 78.8% 28,961 71.2% — — 579 (2) 33.0% 66,942 39.0% Total 98,020 $ 100.0% 28,485 $ 100.0% 40,688 $ 100.0% 2,629 $ 100.0% 1,757 $ 100.0% 171,579 $ 100.0% RENTAL UNCONSOLIDATED INCO ME FINANCING REC OTHER NOTES INCOME INTEREST INCOME MO RTGAGE LOANS ANNUALIZED INCOME JV INCOME GAAP NOI(1 ) MORTGAGE LOANS WA GAAP % OF NOTES WA GAAP % OF % OF YEAR RECEIVABLE RATE TOTAL RECEIVABLE RATE TOTAL TOTAL 2025 15,956 $ 7.9% 4.0% — $ — — 15,956 $ 3.8% 2026 27,237 9.0% 6.9% 25 8.0% 0.1% 27,262 6.5% 2027 — — — 25,000 12.7% 92.6% 25,000 5.9% 2028 — — — 1,029 — 3.8% 1,029 0.3% 2029 — — — — — — — — 2030 95,857 8.4% 24.4% 957 7.6% 3.5% 96,814 23.0% 2031 — — — — — — — — 2032 — — — — — — — — Thereafter 254,537 11.4% 64.7% — — — 254,537 60.5% Total 393,587 $ 10.3% 100.0% 27,011 $ 12.0% 100.0% 420,598 $ 100.0% RECEIVABLE TOTAL LOANS LOANS RECEIVABLE PRINCIPAL MATURITIES |

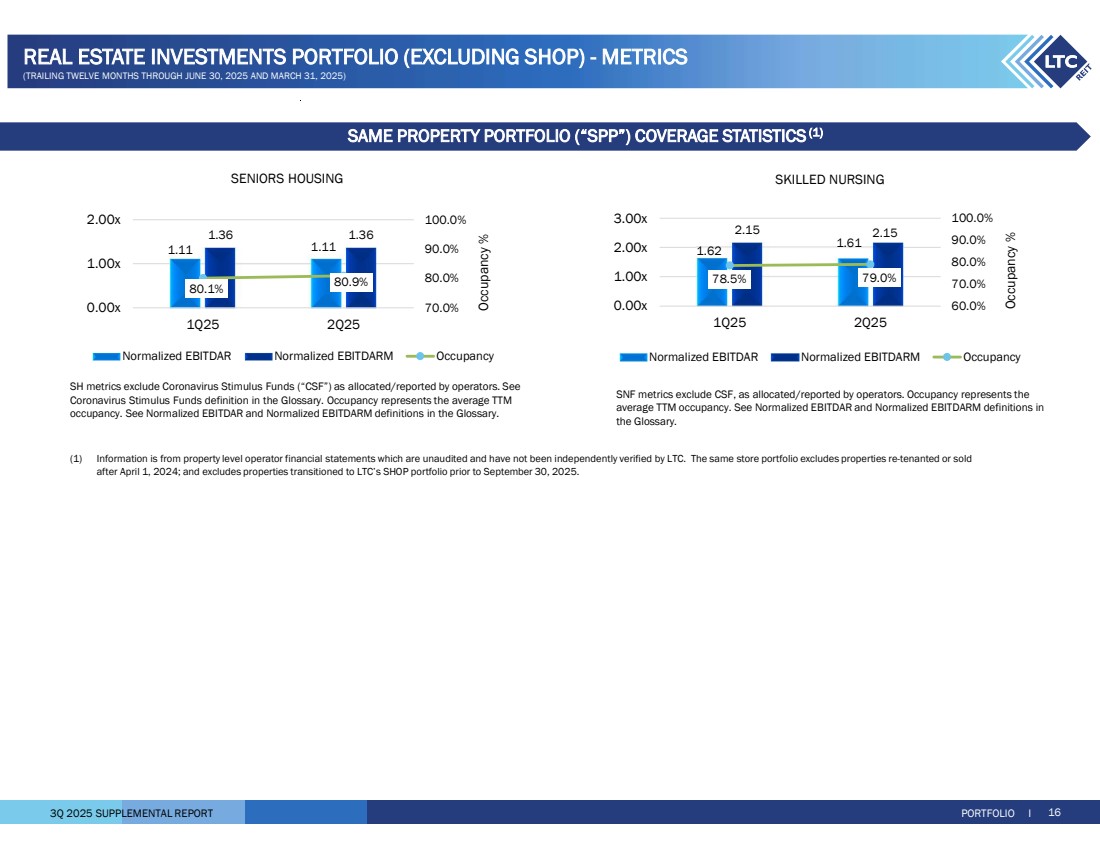

| 3Q 2025 SUPPLEMENTAL REPORT (1) Information is from property level operator financial statements which are unaudited and have not been independently verified by LTC. The same store portfolio excludes properties re-tenanted or sold after April 1, 2024; and excludes properties transitioned to LTC’s SHOP portfolio prior to September 30, 2025. SENIORS HOUSING SKILLED NURSING 1.62 1.61 2.15 2.15 78.5% 79.0% 60.0% 70.0% 80.0% 90.0% 100.0% 0.00x 1.00x 2.00x 3.00x 1Q25 2Q25 Occupancy % Normalized EBITDAR Normalized EBITDARM Occupancy 1.11 1.11 1.36 1.36 80.1% 80.9% 70.0% 80.0% 90.0% 100.0% 0.00x 1.00x 2.00x 1Q25 2Q25 Occupancy % Normalized EBITDAR Normalized EBITDARM Occupancy SNF metrics exclude CSF, as allocated/reported by operators. Occupancy represents the average TTM occupancy. See Normalized EBITDAR and Normalized EBITDARM definitions in the Glossary. SH metrics exclude Coronavirus Stimulus Funds (“CSF”) as allocated/reported by operators. See Coronavirus Stimulus Funds definition in the Glossary. Occupancy represents the average TTM occupancy. See Normalized EBITDAR and Normalized EBITDARM definitions in the Glossary. PORTFOLIO I 16 REAL ESTATE INVESTMENTS PORTFOLIO (EXCLUDING SHOP) - METRICS (TRAILING TWELVE MONTHS THROUGH JUNE 30, 2025 AND MARCH 31, 2025) SAME PROPERTY PORTFOLIO (“SPP”) COVERAGE STATISTICS(1) |

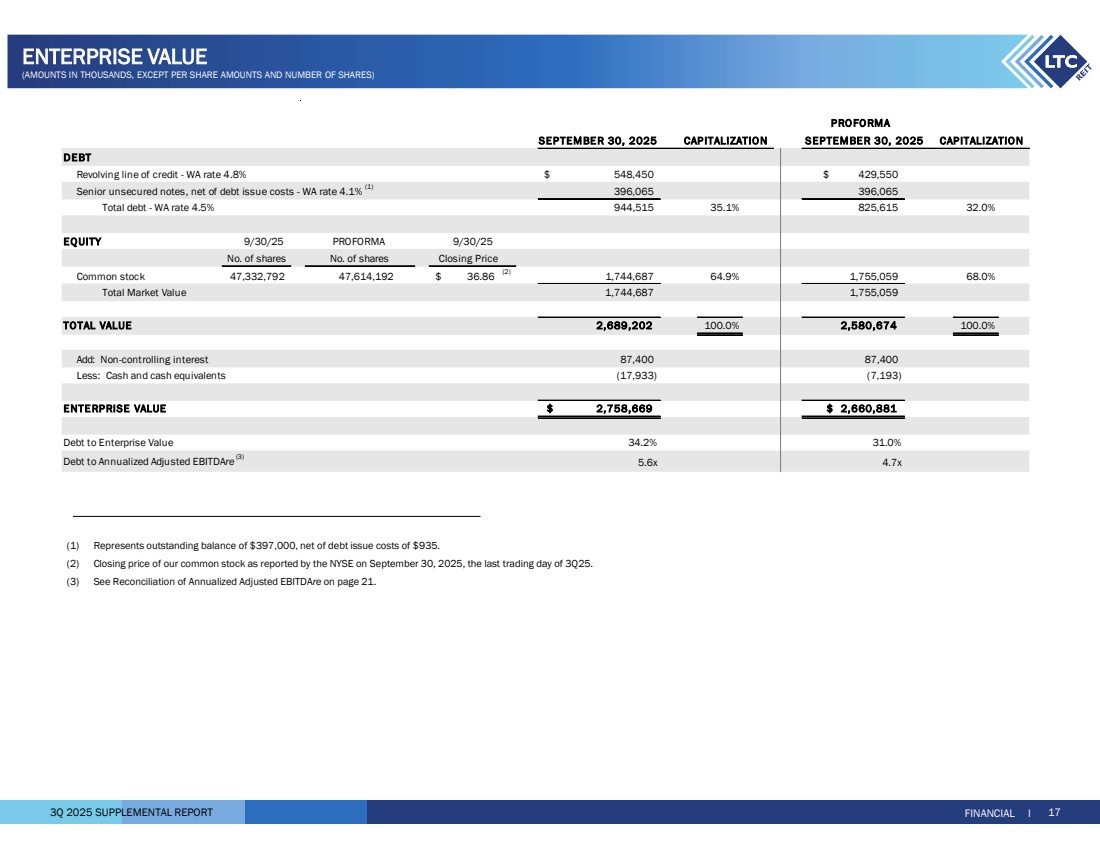

| 3Q 2025 SUPPLEMENTAL REPORT PRO FORMA SEPTEMBE R 30, 2025 Revolving line of credit - WA rate 4.8% 548,450 $ 429,550 $ Senior unsecured notes, net of debt issue costs - WA rate 4.1% (1) 396,065 396,065 Total debt - WA rate 4.5% 944,515 35.1% 825,615 32.0% No. of shares Closing Price Common stock 47,332,792 47,614,192 36.86 $ (2) 64.9% 1,755,059 1,744,687 68.0% Total Market Value 1,744,687 1,755,059 2,689,202 100.0% 2,580,674 100.0% Add: Non-controlling interest 87,400 87,400 Less: Cash and cash equivalents (17,933) (7,193) $ 2,660,881 2,758,669 $ Debt to Enterprise Value 34.2% 31.0% Debt to Annualized Adjusted EBITDAre (3) 5.6x 4.7x PROFORMA No. of shares 9/30/25 CAPITALIZATION SEPTEMBE R 30, 2025 CAPITALIZATION DEBT EQUITY 9/30/25 TOTAL VALUE ENTE RPRISE VALUE FINANCIAL I 17 ENTERPRISE VALUE (AMOUNTS IN THOUSANDS, EXCEPT PER SHARE AMOUNTS AND NUMBER OF SHARES) (1) Represents outstanding balance of $397,000, net of debt issue costs of $935. (2) Closing price of our common stock as reported by the NYSE on September 30, 2025, the last trading day of 3Q25. (3) See Reconciliation of Annualized Adjusted EBITDAre on page 21. |

| 3Q 2025 SUPPLEMENTAL REPORT LEVERAGE RATIOS COVERAGE RATIOS LINE OF CREDIT LIQUIDITY FINANCIAL I 18 DEBT METRICS (DOLLAR AMOUNTS IN THOUSANDS) $130,000 $302,250 $144,350 $548,450 $429,550 $270,000 $97,750 $280,650 $51,550 $170,450 $- $100,000 $200,000 $300,000 $400,000 $500,000 $600,000 2022 2023 2024 3Q25 3Q25 PROFORMA Balance Available (1) See Proforma Activities page for additional proforma information. (1) 37.4% 39.5% 31.1% 38.1% 34.2% 34.1% 39.0% 29.3% 34.2% 31.0% 0.0% 10.0% 20.0% 30.0% 40.0% 50.0% 2022 2023 2024 3Q25 3Q25 PROFORMA Debt to Gross Asset Value Debt to Total Enterprise Value 5.6x 5.6x 4.2x 5.6x 4.7x 4.3x 3.4x 4.0x 4.8x 4.6x 0.0x 2.0x 4.0x 6.0x 8.0x 2022 2023 2024 3Q25 3Q25 PROFORMA Debt to Annualized Adjusted EBITDAre Annualized Adjusted EBITDAre/ Fixed Charges |

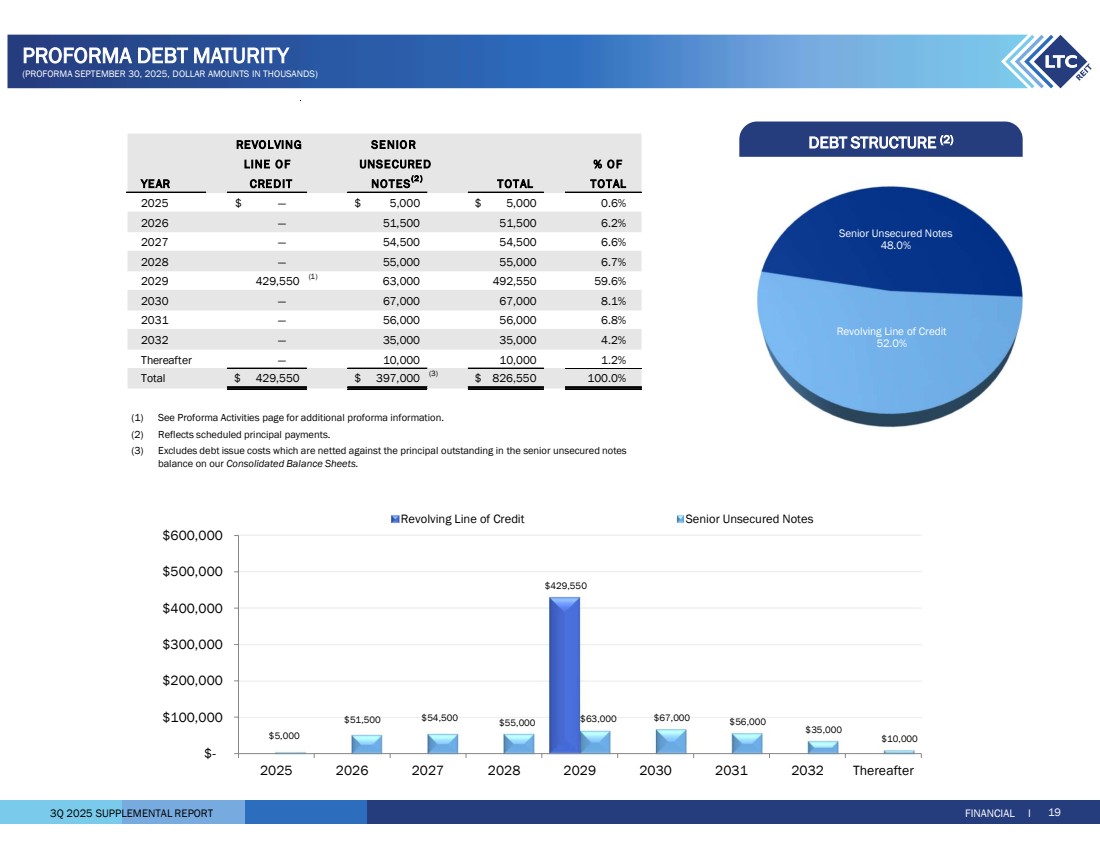

| 3Q 2025 SUPPLEMENTAL REPORT REVOLVING SENIOR LINE OF UNSECURED % OF YEAR CREDIT NOTES(2 ) TOTAL TOTAL 2025 — $ 5,000 $ 5,000 $ 0.6% 2026 — 51,500 51,500 6.2% 2027 — 54,500 54,500 6.6% 2028 — 55,000 55,000 6.7% 2029 429,550 (1) 492,550 63,000 59.6% 2030 — 67,000 67,000 8.1% 2031 — 56,000 56,000 6.8% 2032 — 35,000 35,000 4.2% Thereafter — 10,000 10,000 1.2% Total 429,550 $ 397,000 $ (3) $ 100.0% 826,550 $429,550 $5,000 $51,500 $54,500 $55,000 $63,000 $67,000 $56,000 $35,000 $10,000 $- $100,000 $200,000 $300,000 $400,000 $500,000 $600,000 2025 2026 2027 2028 2029 2030 2031 2032 Thereafter Revolving Line of Credit Senior Unsecured Notes Senior Unsecured Notes 48.0% Revolving Line of Credit 52.0% DEBT STRUCTURE (2) FINANCIAL I 19 PROFORMA DEBT MATURITY (PROFORMA SEPTEMBER 30, 2025, DOLLAR AMOUNTS IN THOUSANDS) (1) See Proforma Activities page for additional proforma information. (2) Reflects scheduled principal payments. (3) Excludes debt issue costs which are netted against the principal outstanding in the senior unsecured notes balance on our Consolidated Balance Sheets. |

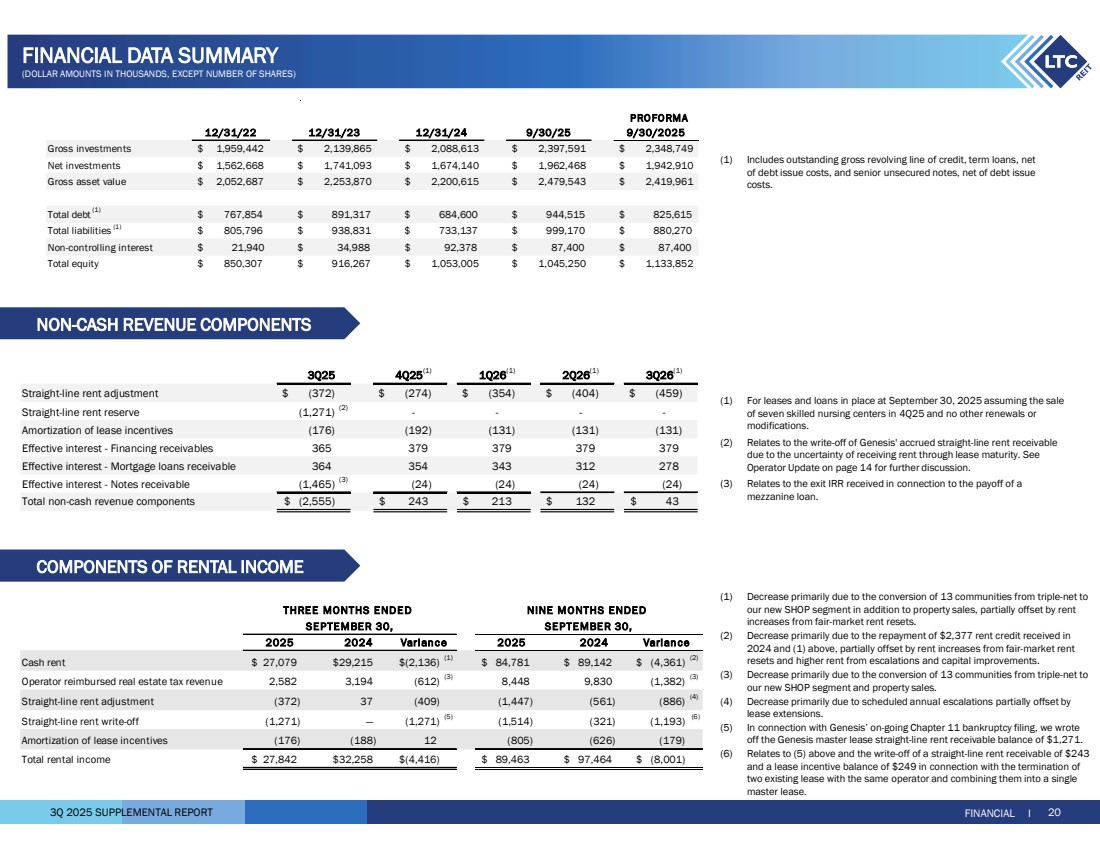

| 3Q 2025 SUPPLEMENTAL REPORT (1) For leases and loans in place at September 30, 2025 assuming the sale of seven skilled nursing centers in 4Q25 and no other renewals or modifications. (2) Relates to the write-off of Genesis' accrued straight-line rent receivable due to the uncertainty of receiving rent through lease maturity. See Operator Update on page 14 for further discussion. (3) Relates to the exit IRR received in connection to the payoff of a mezzanine loan. (1) Decrease primarily due to the conversion of 13 communities from triple-net to our new SHOP segment in addition to property sales, partially offset by rent increases from fair-market rent resets. (2) Decrease primarily due to the repayment of $2,377 rent credit received in 2024 and (1) above, partially offset by rent increases from fair-market rent resets and higher rent from escalations and capital improvements. (3) Decrease primarily due to the conversion of 13 communities from triple-net to our new SHOP segment and property sales. (4) Decrease primarily due to scheduled annual escalations partially offset by lease extensions. (5) In connection with Genesis’ on-going Chapter 11 bankruptcy filing, we wrote off the Genesis master lease straight-line rent receivable balance of $1,271. (6) Relates to (5) above and the write-off of a straight-line rent receivable of $243 and a lease incentive balance of $249 in connection with the termination of two existing lease with the same operator and combining them into a single master lease. COMPONENTS OF RENTAL INCOME FINANCIAL I 20 FINANCIAL DATA SUMMARY (DOLLAR AMOUNTS IN THOUSANDS, EXCEPT NUMBER OF SHARES) 12/31/22 12/31/23 12/31/24 9/30/25 PRO FORMA 9/30/2025 Gross investments $ 1,959,442 $ 2,139,865 $ 2,088,613 $ 2,397,591 $ 2,348,749 Net investments $ 1,562,668 $ 1,741,093 $ 1,674,140 $ 1,962,468 $ 1,942,910 Gross asset value $ 2,052,687 $ 2,253,870 $ 2,200,615 $ 2,479,543 $ 2,419,961 Total debt (1) $ 767,854 $ 891,317 $ 684,600 $ 944,515 $ 825,615 Total liabilities (1) $ 805,796 $ 938,831 $ 733,137 $ 999,170 $ 880,270 Non-controlling interest $ 21,940 $ 34,988 $ 92,378 $ 87,400 $ 87,400 Total equity $ 850,307 $ 916,267 $ 1,053,005 $ 1,045,250 $ 1,133,852 Cash rent 27,079 $ 29,215 $ (2,136) $ (1) $ 89,142 84,781 $ (4,361) $ (2) Operator reimbursed real estate tax revenue 2,582 3,194 (612) (3) 8,448 9,830 (1,382) (3) Straight-line rent adjustment (372) 37 (409) (1,447) (561) (886) (4) Straight-line rent write-off (1,271) — (1,271) (5) (321) (1,514) (1,193) (6) Amortization of lease incentives (176) (188) 12 (805) (626) (179) Total rental income 27,842 $ 32,258 $ (4,416) $ 89,463 $ 97,464 $ (8,001) $ Varian ce THREE MONTHS ENDED NINE MONTHS ENDED SEPTEMBER 30, SEPTEMBER 30, 2025 2024 2025 2024 Varianc e (1) Includes outstanding gross revolving line of credit, term loans, net of debt issue costs, and senior unsecured notes, net of debt issue costs. NON-CASH REVENUE COMPONENTS 3Q25 4Q25(1) 1Q26(1) 2Q26(1) 3Q26(1) $ (274) (372) $ (354) $ (404) $ (459) $ Straight-line rent reserve (1,271) (2) - - - - Amortization of lease incentives (176) (192) (131) (131) (131) 379 365 379 379 379 Effective interest - Mortgage loans receivable 364 354 343 312 278 (1,465) (3) (24) (24) (24) (24) $ 243 (2,555) $ 213 $ 132 $ 43 $ Straight-line rent adjustment Effective interest - Financing receivables Effective interest - Notes receivable Total non-cash revenue components |

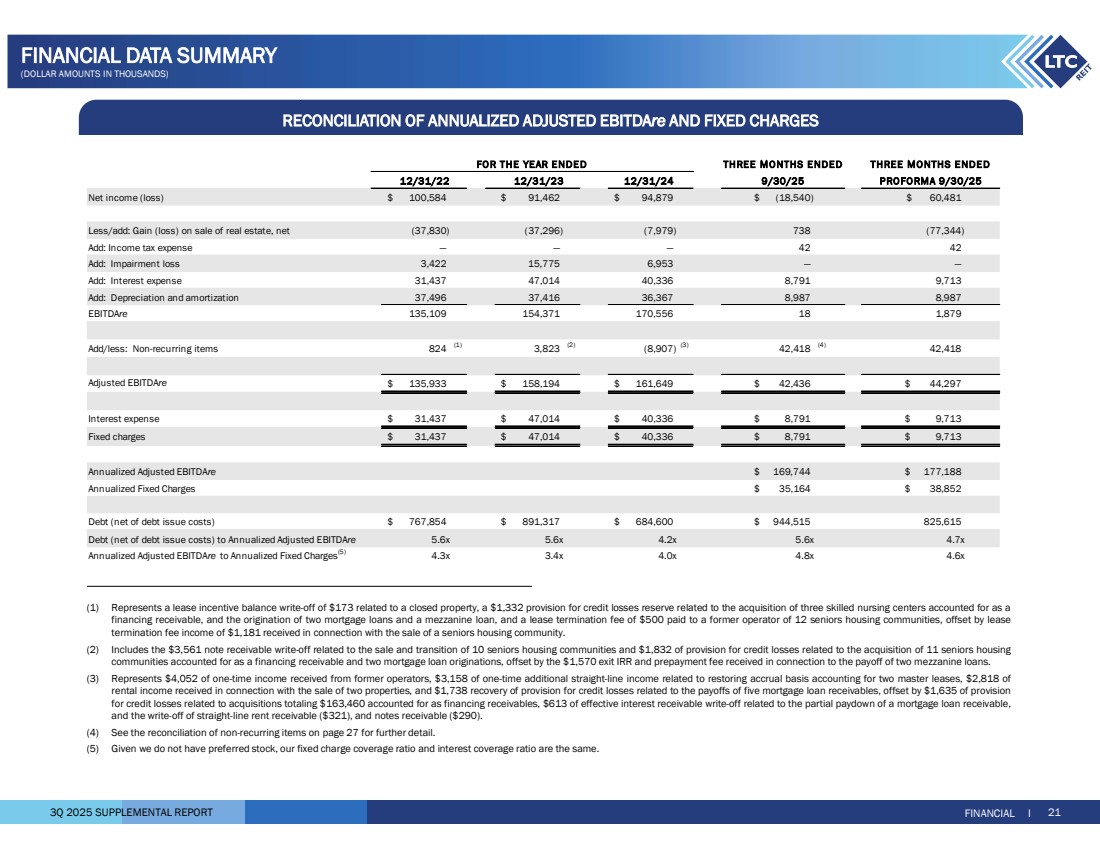

| 3Q 2025 SUPPLEMENTAL REPORT RECONCILIATION OF ANNUALIZED ADJUSTED EBITDAre AND FIXED CHARGES FINANCIAL I 21 FINANCIAL DATA SUMMARY (DOLLAR AMOUNTS IN THOUSANDS) 12/31/24 Net income (loss) 100,584 $ 91,462 $ 94,879 $ (18,540) $ 60,481 $ Less/add: Gain (loss) on sale of real estate, net (37,830) (37,296) (7,979) 738 (77,344) Add: Income tax expense — — — 42 42 Add: Impairment loss 3,422 15,775 6,953 — — Add: Interest expense 31,437 47,014 40,336 8,791 9,713 Add: Depreciation and amortization 37,496 37,416 36,367 8,987 8,987 EBITDAre 154,371 135,109 170,556 18 1,879 Add/less: Non-recurring items 824 (1) 3,823 (2) (8,907) (3) 42,418 (4) 42,418 Adjusted EBITDAre $ 158,194 135,933 $ 161,649 $ 42,436 $ 44,297 $ Interest expense 31,437 $ 47,014 $ 40,336 $ 8,791 $ 9,713 $ Fixed charges 31,437 $ 47,014 $ 40,336 $ 8,791 $ 9,713 $ Annualized Adjusted EBITDAre $ 177,188 169,744 $ Annualized Fixed Charges 35,164 $ 38,852 $ Debt (net of debt issue costs) 767,854 $ 891,317 $ 684,600 $ 944,515 $ 825,615 Debt (net of debt issue costs) to Annualized Adjusted EBITDAre 5.6x 5.6x 4.2x 5.6x 4.7x Annualized Adjusted EBITDAre to Annualized Fixed Charges(5) 4.3x 3.4x 4.0x 4.8x 4.6x FOR THE YEAR ENDED THREE MONTHS ENDED THREE MONTHS ENDED 12/31/22 12/31/23 9/30/25 PROFORMA 9/30/25 (1) Represents a lease incentive balance write-off of $173 related to a closed property, a $1,332 provision for credit losses reserve related to the acquisition of three skilled nursing centers accounted for as a financing receivable, and the origination of two mortgage loans and a mezzanine loan, and a lease termination fee of $500 paid to a former operator of 12 seniors housing communities, offset by lease termination fee income of $1,181 received in connection with the sale of a seniors housing community. (2) Includes the $3,561 note receivable write-off related to the sale and transition of 10 seniors housing communities and $1,832 of provision for credit losses related to the acquisition of 11 seniors housing communities accounted for as a financing receivable and two mortgage loan originations, offset by the $1,570 exit IRR and prepayment fee received in connection to the payoff of two mezzanine loans. (3) Represents $4,052 of one-time income received from former operators, $3,158 of one-time additional straight-line income related to restoring accrual basis accounting for two master leases, $2,818 of rental income received in connection with the sale of two properties, and $1,738 recovery of provision for credit losses related to the payoffs of five mortgage loan receivables, offset by $1,635 of provision for credit losses related to acquisitions totaling $163,460 accounted for as financing receivables, $613 of effective interest receivable write-off related to the partial paydown of a mortgage loan receivable, and the write-off of straight-line rent receivable ($321), and notes receivable ($290). (4) See the reconciliation of non-recurring items on page 27 for further detail. (5) Given we do not have preferred stock, our fixed charge coverage ratio and interest coverage ratio are the same. |

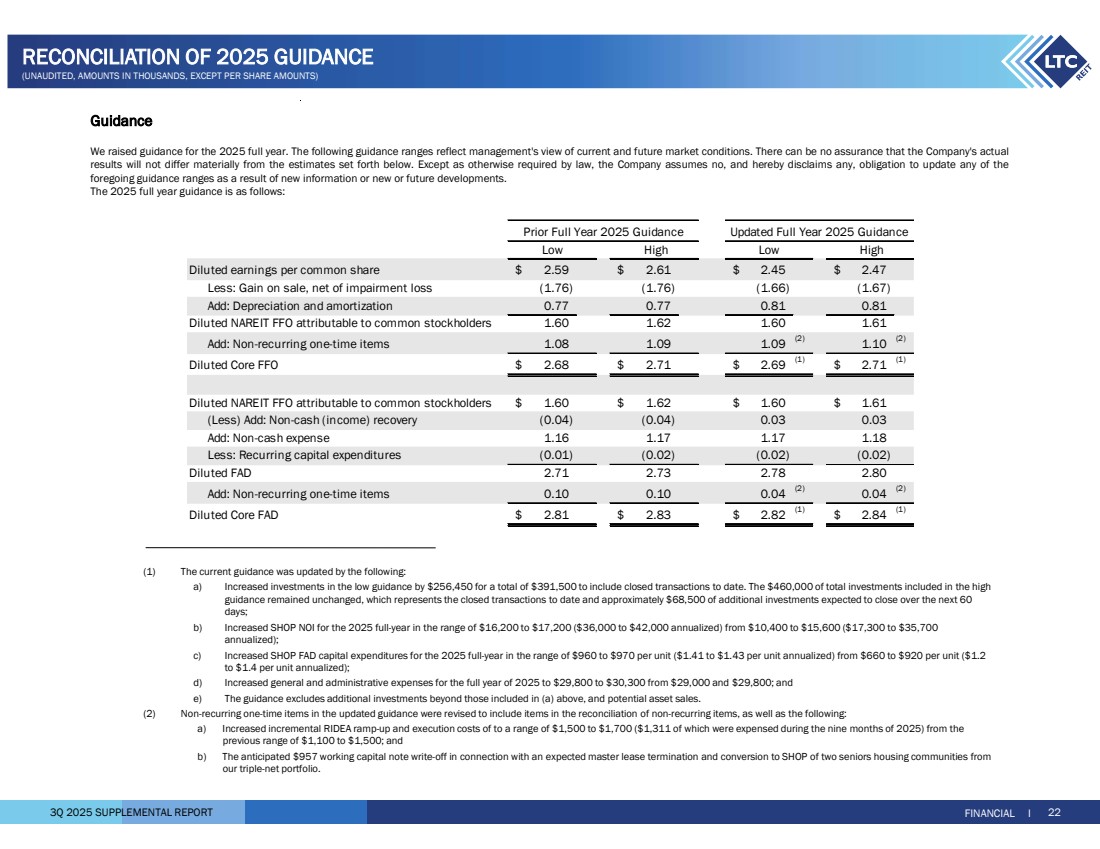

| 3Q 2025 SUPPLEMENTAL REPORT FINANCIAL I 22 RECONCILIATION OF 2025 GUIDANCE (UNAUDITED, AMOUNTS IN THOUSANDS, EXCEPT PER SHARE AMOUNTS) Guidance We raised guidance for the 2025 full year. The following guidance ranges reflect management's view of current and future market conditions. There can be no assurance that the Company's actual results will not differ materially from the estimates set forth below. Except as otherwise required by law, the Company assumes no, and hereby disclaims any, obligation to update any of the foregoing guidance ranges as a result of new information or new or future developments. The 2025 full year guidance is as follows: (1) The current guidance was updated by the following: a) Increased investments in the low guidance by $256,450 for a total of $391,500 to include closed transactions to date. The $460,000 of total investments included in the high guidance remained unchanged, which represents the closed transactions to date and approximately $68,500 of additional investments expected to close over the next 60 days; b) Increased SHOP NOI for the 2025 full-year in the range of $16,200 to $17,200 ($36,000 to $42,000 annualized) from $10,400 to $15,600 ($17,300 to $35,700 annualized); c) Increased SHOP FAD capital expenditures for the 2025 full-year in the range of $960 to $970 per unit ($1.41 to $1.43 per unit annualized) from $660 to $920 per unit ($1.2 to $1.4 per unit annualized); d) Increased general and administrative expenses for the full year of 2025 to $29,800 to $30,300 from $29,000 and $29,800; and e) The guidance excludes additional investments beyond those included in (a) above, and potential asset sales. (2) Non-recurring one-time items in the updated guidance were revised to include items in the reconciliation of non-recurring items, as well as the following: a) Increased incremental RIDEA ramp-up and execution costs of to a range of $1,500 to $1,700 ($1,311 of which were expensed during the nine months of 2025) from the previous range of $1,100 to $1,500; and b) The anticipated $957 working capital note write-off in connection with an expected master lease termination and conversion to SHOP of two seniors housing communities from our triple-net portfolio. Low High Low High Diluted earnings per common share 2.59 $ 2.61 $ 2.45 $ 2.47 $ Less: Gain on sale, net of impairment loss (1.76) (1.76) (1.66) (1.67) Add: Depreciation and amortization 0.77 0.77 0.81 0.81 Diluted NAREIT FFO attributable to common stockholders 1.60 1.62 1.60 1.61 Add: Non-recurring one-time items 1.08 1.09 1.09 (2) 1.10 (2) Diluted Core FFO 2.68 $ 2.71 $ 2.69 $ (1) $ 2.71 (1) Diluted NAREIT FFO attributable to common stockholders 1.60 $ 1.62 $ 1.60 $ 1.61 $ (Less) Add: Non-cash (income) recovery (0.04) (0.04) 0.03 0.03 Add: Non-cash expense 1.16 1.17 1.17 1.18 Less: Recurring capital expenditures (0.01) (0.02) (0.02) (0.02) Diluted FAD 2.71 2.73 2.78 2.80 Add: Non-recurring one-time items 0.10 0.10 0.04 (2) 0.04 (2) Diluted Core FAD 2.81 $ 2.83 $ 2.82 $ (1) $ 2.84 (1) Prior Full Year 2025 Guidance Updated Full Year 2025 Guidance |

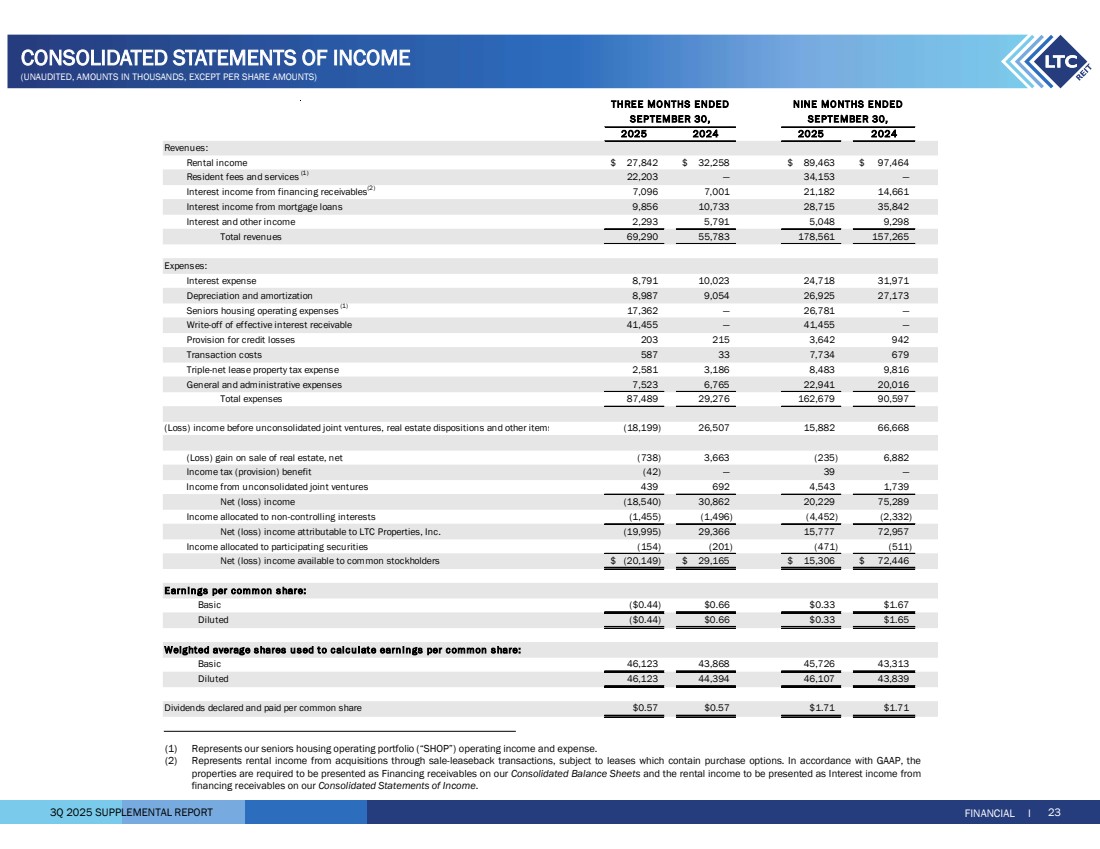

| 3Q 2025 SUPPLEMENTAL REPORT 2025 2024 2025 2024 Revenues: Rental income 27,842 $ 32,258 $ 89,463 $ 97,464 $ Resident fees and services (1) 22,203 — 34,153 — Interest income from financing receivables(2) 7,096 7,001 21,182 14,661 Interest income from mortgage loans 9,856 10,733 28,715 35,842 Interest and other income 2,293 5,791 5,048 9,298 Total revenues 69,290 55,783 178,561 157,265 Expenses: Interest expense 8,791 10,023 24,718 31,971 Depreciation and amortization 8,987 9,054 26,925 27,173 Seniors housing operating expenses (1) — 17,362 26,781 — Write-off of effective interest receivable 41,455 — 41,455 — Provision for credit losses 203 215 3,642 942 Transaction costs 587 33 7,734 679 Triple-net lease property tax expense 2,581 3,186 8,483 9,816 General and administrative expenses 7,523 6,765 22,941 20,016 Total expenses 87,489 29,276 162,679 90,597 (18,199) 26,507 15,882 66,668 (Loss) gain on sale of real estate, net (738) 3,663 (235) 6,882 Income tax (provision) benefit (42) — 39 — Income from unconsolidated joint ventures 439 692 4,543 1,739 Net (loss) income (18,540) 30,862 20,229 75,289 Income allocated to non-controlling interests (1,455) (1,496) (4,452) (2,332) Net (loss) income attributable to LTC Properties, Inc. (19,995) 29,366 15,777 72,957 Income allocated to participating securities (154) (201) (471) (511) Net (loss) income available to common stockholders (20,149) $ 29,165 $ 15,306 $ 72,446 $ Earnings per common s hare: Basic ($0.44) $0.66 $0.33 $1.67 Diluted ($0.44) $0.66 $0.33 $1.65 Weighted average s hares u sed to c alc ulate earn ings per c ommon s hare: Basic 46,123 43,868 45,726 43,313 Diluted 46,123 44,394 46,107 43,839 Dividends declared and paid per common share $0.57 $0.57 $1.71 $1.71 (Loss) income before unconsolidated joint ventures, real estate dispositions and other items THRE E MO NTHS ENDED SEPTEMBER 30, SEPTE MBER 30, NINE MO NTHS ENDED FINANCIAL I 23 CONSOLIDATED STATEMENTS OF INCOME (UNAUDITED, AMOUNTS IN THOUSANDS, EXCEPT PER SHARE AMOUNTS) (1) Represents our seniors housing operating portfolio (“SHOP”) operating income and expense. (2) Represents rental income from acquisitions through sale-leaseback transactions, subject to leases which contain purchase options. In accordance with GAAP, the properties are required to be presented as Financing receivables on our Consolidated Balance Sheets and the rental income to be presented as Interest income from financing receivables on our Consolidated Statements of Income. |

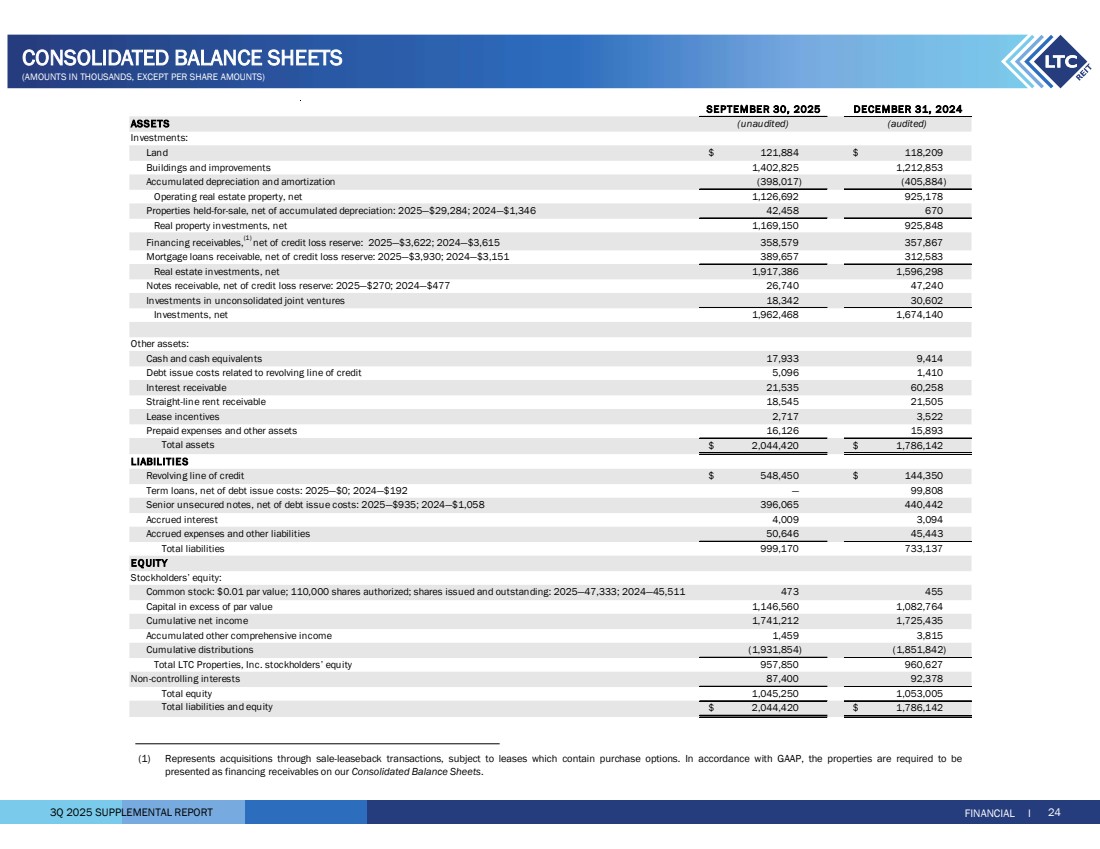

| 3Q 2025 SUPPLEMENTAL REPORT FINANCIAL I 24 CONSOLIDATED BALANCE SHEETS (AMOUNTS IN THOUSANDS, EXCEPT PER SHARE AMOUNTS) ASSETS Investments: Land $ 121,884 $ 118,209 Buildings and improvements 1,402,825 1,212,853 Accumulated depreciation and amortization (398,017) (405,884) Operating real estate property, net 1,126,692 925,178 Properties held-for-sale, net of accumulated depreciation: 2025—$29,284; 2024—$1,346 42,458 670 Real property investments, net 1,169,150 925,848 Financing receivables,(1) net of credit loss reserve: 2025—$3,622; 2024—$3,615 358,579 357,867 Mortgage loans receivable, net of credit loss reserve: 2025—$3,930; 2024—$3,151 389,657 312,583 Real estate investments, net 1,917,386 1,596,298 Notes receivable, net of credit loss reserve: 2025—$270; 2024—$477 26,740 47,240 Investments in unconsolidated joint ventures 18,342 30,602 Investments, net 1,962,468 1,674,140 Other assets: Cash and cash equivalents 17,933 9,414 Debt issue costs related to revolving line of credit 5,096 1,410 Interest receivable 21,535 60,258 Straight-line rent receivable 18,545 21,505 Lease incentives 2,717 3,522 Prepaid expenses and other assets 16,126 15,893 Total assets $ 2,044,420 $ 1,786,142 LIABILITIES Revolving line of credit $ 548,450 $ 144,350 Term loans, net of debt issue costs: 2025—$0; 2024—$192 — 99,808 Senior unsecured notes, net of debt issue costs: 2025—$935; 2024—$1,058 396,065 440,442 Accrued interest 4,009 3,094 Accrued expenses and other liabilities 50,646 45,443 Total liabilities 999,170 733,137 EQ UITY Stockholders’ equity: Common stock: $0.01 par value; 110,000 shares authorized; shares issued and outstanding: 2025—47,333; 2024—45,511 473 455 Capital in excess of par value 1,146,560 1,082,764 Cumulative net income 1,741,212 1,725,435 Accumulated other comprehensive income 1,459 3,815 Cumulative distributions (1,931,854) (1,851,842) Total LTC Properties, Inc. stockholders’ equity 957,850 960,627 Non-controlling interests 87,400 92,378 Total equity 1,045,250 1,053,005 Total liabilities and equity $ 2,044,420 $ 1,786,142 (unaudited) (audited) SEPTEMBER 30, 2025 DECEMBER 31, 2024 (1) Represents acquisitions through sale-leaseback transactions, subject to leases which contain purchase options. In accordance with GAAP, the properties are required to be presented as financing receivables on our Consolidated Balance Sheets. |

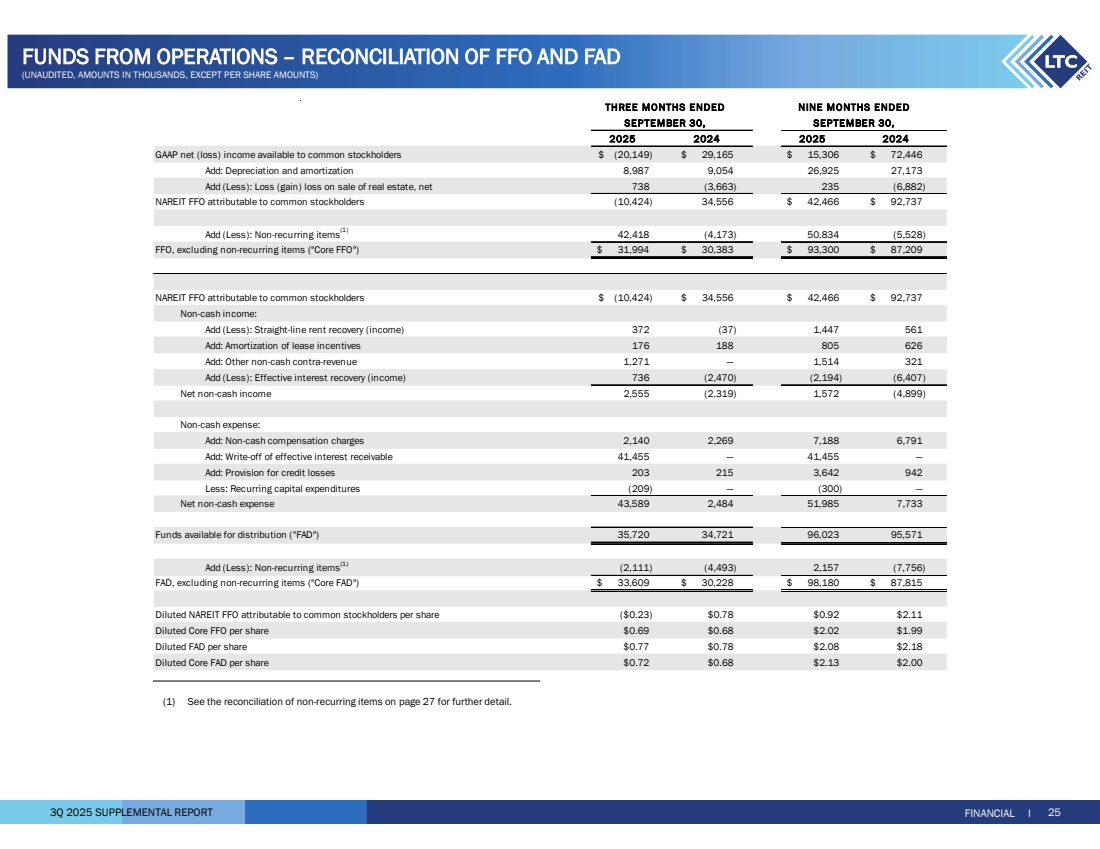

| 3Q 2025 SUPPLEMENTAL REPORT FINANCIAL I 25 FUNDS FROM OPERATIONS – RECONCILIATION OF FFO AND FAD (UNAUDITED, AMOUNTS IN THOUSANDS, EXCEPT PER SHARE AMOUNTS) 2025 2024 2025 2024 GAAP net (loss) income available to common stockholders (20,149) $ 29,165 $ 15,306 $ 72,446 $ Add: Depreciation and amortization 8,987 9,054 26,925 27,173 Add (Less): Loss (gain) loss on sale of real estate, net 738 (3,663) 235 (6,882) NAREIT FFO attributable to common stockholders (10,424) 34,556 42,466 $ 92,737 $ Add (Less): Non-recurring items(1) (4,173) 42,418 50,834 (5,528) $ 30,383 31,994 $ 93,300 $ 87,209 $ NAREIT FFO attributable to common stockholders (10,424) $ 34,556 $ 42,466 $ 92,737 $ Non-cash income: Add (Less): Straight-line rent recovery (income) 372 (37) 1,447 561 Add: Amortization of lease incentives 176 188 805 626 Add: Other non-cash contra-revenue 1,271 — 1,514 321 Add (Less): Effective interest recovery (income) 736 (2,470) (2,194) (6,407) Net non-cash income 2,555 (2,319) 1,572 (4,899) Non-cash expense: Add: Non-cash compensation charges 2,140 2,269 7,188 6,791 Add: Write-off of effective interest receivable 41,455 — 41,455 — Add: Provision for credit losses 203 215 3,642 942 Less: Recurring capital expenditures (209) — (300) — Net non-cash expense 43,589 2,484 51,985 7,733 Funds available for distribution ("FAD") 35,720 34,721 96,023 95,571 Add (Less): Non-recurring items(1) (4,493) (2,111) 2,157 (7,756) FAD, excluding non-recurring items ("Core FAD") 33,609 $ 30,228 $ 98,180 $ 87,815 $ ($0.23) $0.78 $0.92 $2.11 $0.69 $0.68 $2.02 $1.99 $0.77 $0.78 $2.08 $2.18 $0.72 $0.68 $2.13 $2.00 THREE MONTHS ENDED NINE MONTHS ENDED SEPTEMBER 30, SEPTEMBER 30, Diluted NAREIT FFO attributable to common stockholders per share Diluted Core FFO per share Diluted FAD per share Diluted Core FAD per share FFO, excluding non-recurring items ("Core FFO") (1) See the reconciliation of non-recurring items on page 27 for further detail. |

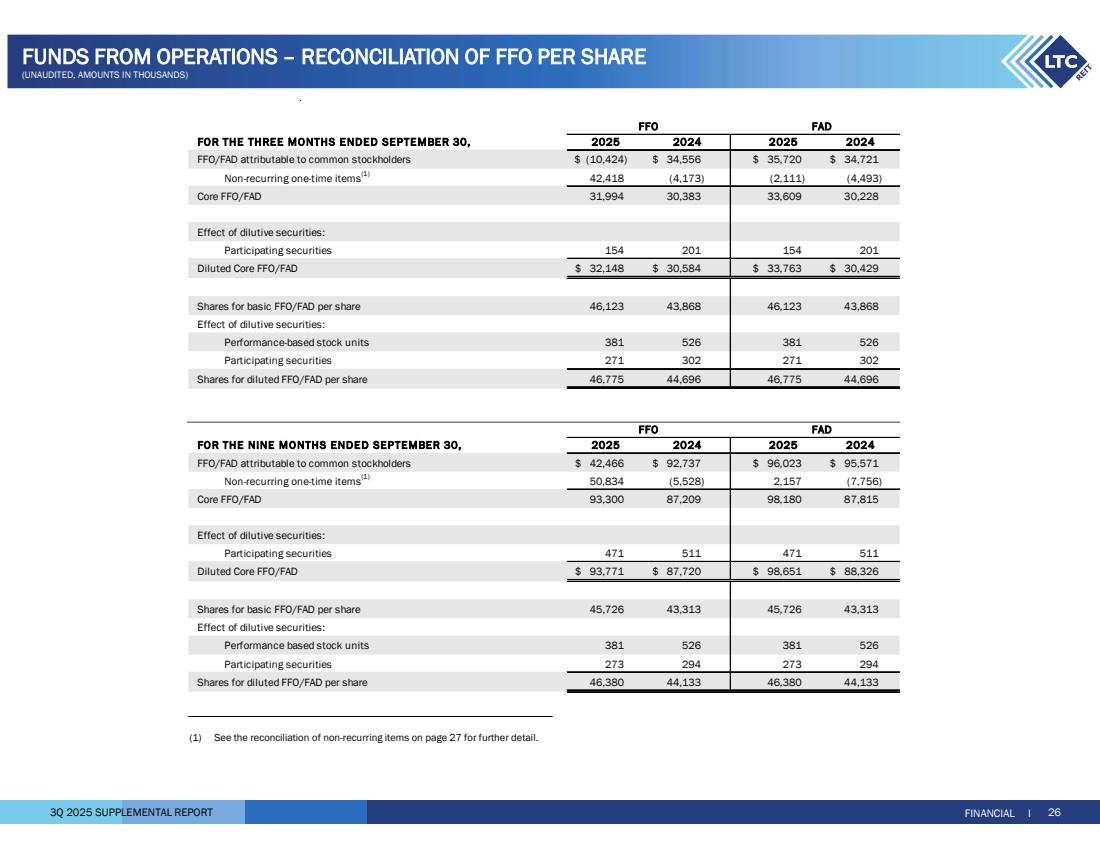

| 3Q 2025 SUPPLEMENTAL REPORT FOR THE THREE MONTHS ENDED SEPTE MBER 30, FFO/FAD attributable to common stockholders (10,424) $ 34,556 $ 35,720 $ 34,721 $ Non-recurring one-time items(1) (4,173) 42,418 (2,111) (4,493) Core FFO/FAD 31,994 30,383 33,609 30,228 Effect of dilutive securities: Participating securities 154 201 154 201 Diluted Core FFO/FAD 32,148 $ 30,584 $ 33,763 $ 30,429 $ 43,868 46,123 46,123 43,868 Effect of dilutive securities: Performance-based stock units 381 526 381 526 Participating securities 271 302 271 302 Shares for diluted FFO/FAD per share 46,775 44,696 46,775 44,696 FOR THE NINE MONTHS ENDED SEPTEMBER 30, FFO/FAD attributable to common stockholders 42,466 $ 92,737 $ 96,023 $ 95,571 $ Non-recurring one-time items(1) (5,528) 50,834 2,157 (7,756) Core FFO/FAD 93,300 87,209 98,180 87,815 Effect of dilutive securities: Participating securities 471 511 471 511 Diluted Core FFO/FAD 93,771 $ 87,720 $ 98,651 $ 88,326 $ 43,313 45,726 45,726 43,313 Effect of dilutive securities: Performance based stock units 381 526 381 526 Participating securities 273 294 273 294 Shares for diluted FFO/FAD per share 46,380 44,133 46,380 44,133 Shares for basic FFO/FAD per share 2025 2024 2024 Shares for basic FFO/FAD per share FFO FAD 2025 FFO FAD 2025 2024 2025 2024 FINANCIAL I 26 FUNDS FROM OPERATIONS – RECONCILIATION OF FFO PER SHARE (UNAUDITED, AMOUNTS IN THOUSANDS) (1) See the reconciliation of non-recurring items on page 27 for further detail. |

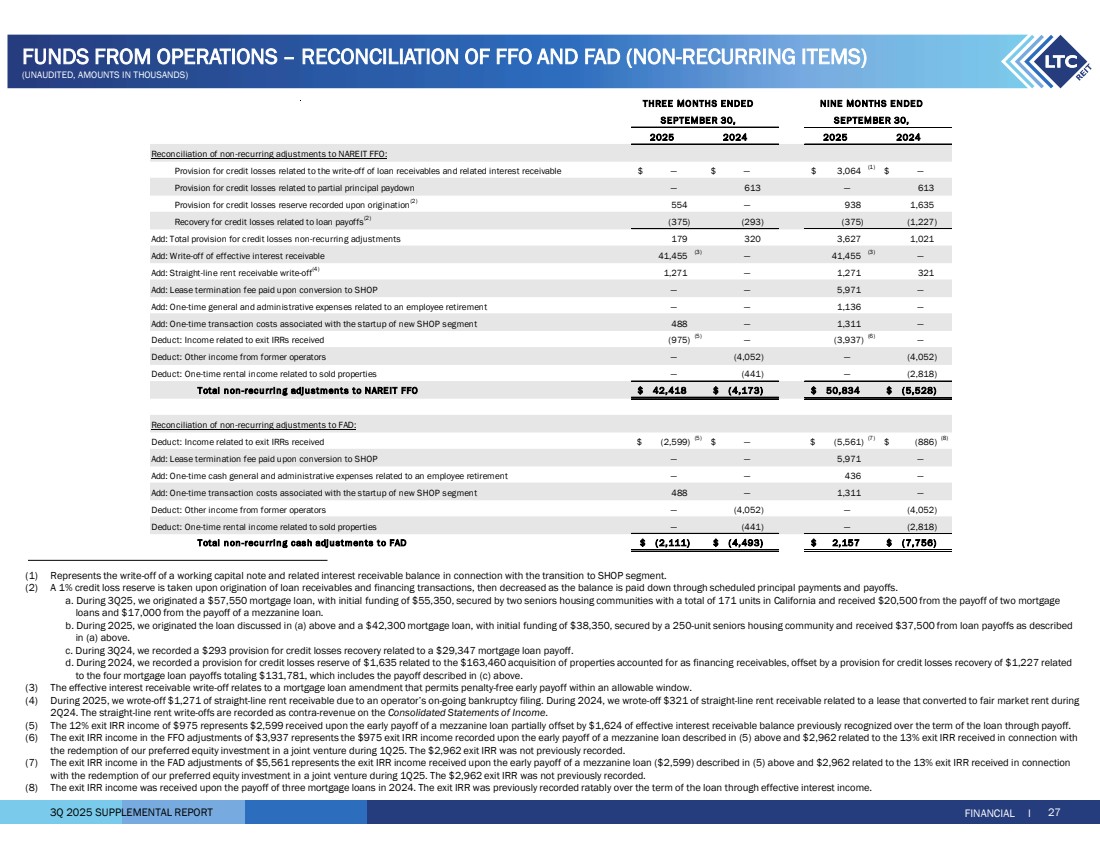

| 3Q 2025 SUPPLEMENTAL REPORT 2025 2024 2025 2024 Reconciliation of non-recurring adjustments to NAREIT FFO: Provision for credit losses related to the write-off of loan receivables and related interest receivable — $ — $ 3,064 $ (1) $ — Provision for credit losses related to partial principal paydown — 613 — 613 Provision for credit losses reserve recorded upon origination(2) — 554 938 1,635 Recovery for credit losses related to loan payoffs(2) (293) (375) (375) (1,227) Add: Total provision for credit losses non-recurring adjustments 179 320 3,627 1,021 Add: Write-off of effective interest receivable 41,455 (3) 41,455 — (3) — Add: Straight-line rent receivable write-off(4) — 1,271 1,271 321 Add: Lease termination fee paid upon conversion to SHOP — — 5,971 — Add: One-time general and administrative expenses related to an employee retirement — — 1,136 — Add: One-time transaction costs associated with the startup of new SHOP segment 488 — 1,311 — Deduct: Income related to exit IRRs received (975) (5) (3,937) — (6) — Deduct: Other income from former operators — (4,052) — (4,052) Deduct: One-time rental income related to sold properties — (441) — (2,818) Total n on -recu rrin g adju stment s to NAREIT FFO 42,418 $ ( 4,173) $ 50,834 $ ( 5,528) $ Reconciliation of non-recurring adjustments to FAD: Deduct: Income related to exit IRRs received (2,599) $ (5) $ (5,561) — $ (7) $ (886) (8) Add: Lease termination fee paid upon conversion to SHOP — — 5,971 — Add: One-time cash general and administrative expenses related to an employee retirement — — 436 — Add: One-time transaction costs associated with the startup of new SHOP segment 488 — 1,311 — Deduct: Other income from former operators — (4,052) — (4,052) Deduct: One-time rental income related to sold properties — (441) — (2,818) Total n on -recu rrin g cas h adju stmen ts to FAD ( 2,111) $ ( 4,493) $ 2,157 $ ( 7,756) $ SEPTEMBER 30, THREE MO NTHS ENDED NINE MO NTHS ENDED SEPTEMBER 30, FINANCIAL I 27 FUNDS FROM OPERATIONS – RECONCILIATION OF FFO AND FAD (NON-RECURRING ITEMS) (UNAUDITED, AMOUNTS IN THOUSANDS) (1) Represents the write-off of a working capital note and related interest receivable balance in connection with the transition to SHOP segment. (2) A 1% credit loss reserve is taken upon origination of loan receivables and financing transactions, then decreased as the balance is paid down through scheduled principal payments and payoffs. a. During 3Q25, we originated a $57,550 mortgage loan, with initial funding of $55,350, secured by two seniors housing communities with a total of 171 units in California and received $20,500 from the payoff of two mortgage loans and $17,000 from the payoff of a mezzanine loan. b. During 2025, we originated the loan discussed in (a) above and a $42,300 mortgage loan, with initial funding of $38,350, secured by a 250-unit seniors housing community and received $37,500 from loan payoffs as described in (a) above. c. During 3Q24, we recorded a $293 provision for credit losses recovery related to a $29,347 mortgage loan payoff. d. During 2024, we recorded a provision for credit losses reserve of $1,635 related to the $163,460 acquisition of properties accounted for as financing receivables, offset by a provision for credit losses recovery of $1,227 related to the four mortgage loan payoffs totaling $131,781, which includes the payoff described in (c) above. (3) The effective interest receivable write-off relates to a mortgage loan amendment that permits penalty-free early payoff within an allowable window. (4) During 2025, we wrote-off $1,271 of straight-line rent receivable due to an operator’s on-going bankruptcy filing. During 2024, we wrote-off $321 of straight-line rent receivable related to a lease that converted to fair market rent during 2Q24. The straight-line rent write-offs are recorded as contra-revenue on the Consolidated Statements of Income. (5) The 12% exit IRR income of $975 represents $2,599 received upon the early payoff of a mezzanine loan partially offset by $1,624 of effective interest receivable balance previously recognized over the term of the loan through payoff. (6) The exit IRR income in the FFO adjustments of $3,937 represents the $975 exit IRR income recorded upon the early payoff of a mezzanine loan described in (5) above and $2,962 related to the 13% exit IRR received in connection with the redemption of our preferred equity investment in a joint venture during 1Q25. The $2,962 exit IRR was not previously recorded. (7) The exit IRR income in the FAD adjustments of $5,561 represents the exit IRR income received upon the early payoff of a mezzanine loan ($2,599) described in (5) above and $2,962 related to the 13% exit IRR received in connection with the redemption of our preferred equity investment in a joint venture during 1Q25. The $2,962 exit IRR was not previously recorded. (8) The exit IRR income was received upon the payoff of three mortgage loans in 2024. The exit IRR was previously recorded ratably over the term of the loan through effective interest income. |

| 3Q 2025 SUPPLEMENTAL REPORT Annualized Contractual Cash NOI: Represents annualized contractual cash rental income (prior to abatements & deferred rent repayment and excludes real estate tax reimbursement), interest income from financing receivables, mortgage loans, mezzanine loans and working capital notes, and income from unconsolidated joint ventures for the final month of the quarter reported herein. Also, represents annualized projected SHOP net operating income for the quarter reported herein. Annualized GAAP NOI: Represents annualized GAAP rent which includes contractual cash rent, straight-line rent and amortization of lease incentives and excludes real estate tax reimbursement, GAAP interest income from financing receivables, mortgage loans, mezzanine loans and working capital notes, and income from unconsolidated joint ventures for the final month of the quarter reported herein. Also, represents annualized projected SHOP net operating income for the quarter reported herein. Assisted Living Communities (“ALF”): The ALF portfolio consists of assisted living, independent living, and/or memory care properties. (See Independent Living and Memory Care) Assisted living properties are seniors housing properties serving elderly persons who require assistance with activities of daily living, but do not require the constant supervision skilled nursing properties provide. Services are usually available 24 hours a day and include personal supervision and assistance with eating, bathing, grooming and administering medication. The facilities provide a combination of housing, supportive services, personalized assistance and health care designed to respond to individual needs. Contractual Lease Rent: Rental revenue as defined by the lease agreement between us and the operator for the lease year. Coronavirus Stimulus Funds (“CSF”): CSF includes funding from various state and federal programs to support healthcare providers in dealing with the challenges of the coronavirus pandemic. Included in CSF are state-specific payments identified by operators as well as federal payments connected to the Paycheck Protection Program and the Provider Relief Fund. CSF is self-reported by operators in unaudited financial statements provided to LTC. Specifically excluded from CSF are the suspension of the Medicare sequestration cut, and increases to the Federal Medical Assistance Percentages (FMAP), both of which are reflected in reported coverage both including and excluding CSF. Earnings Before Interest, Tax, Depreciation and Amortization for Real Estate (“EBITDAre”): As defined by the National Association of Real Estate Investment Trusts (“NAREIT”), EBITDAre is calculated as net income (computed in accordance with GAAP) excluding (i) interest expense, (ii) income tax expense, (iii) real estate depreciation and amortization, (iv) impairment write-downs of depreciable real estate, (v) gains or losses on the sale of depreciable real estate, and (vi) adjustments for unconsolidated partnerships and joint ventures. Financing Receivables: Properties acquired through a sale-leaseback transaction with an operating entity being the same before and after the sale-leaseback, subject to a lease contract that contains a purchase option. In accordance with GAAP, the purchased assets are required to be presented as Financing Receivables on our Consolidated Balance Sheets and the rental income to be presented as Interest income from financing receivables on our Consolidated Statements of Income. Funds Available for Distribution (“FAD”): FFO excluding the effects of straight-line rent, amortization of lease costs, effective interest income, provision for credit losses, non-cash compensation charges, non-cash interest charges and recurring capital expenditures required to maintain and re-tenant our properties. Funds From Operations (“FFO”): As defined by NAREIT, net income available to common stockholders (computed in accordance with U.S. GAAP) excluding gains or losses on the sale of real estate and impairment write-downs of depreciable real estate plus real estate depreciation and amortization, and after adjustments for unconsolidated partnerships and joint ventures. GAAP Rent: Total rent we will receive as a fixed amount over the initial term of the lease and recognized evenly over that term. GAAP rent recorded in the early years of a lease is higher than the cash rent received and during the later years of the lease, the cash rent received is higher than GAAP rent recognized. The difference between the cash rent and GAAP rent is commonly referred to as straight-line rental income. GAAP rent also includes amortization of lease incentives and real estate tax reimbursements. Gross Asset Value: The carrying amount of total assets after adding back accumulated depreciation and loan loss reserves, as reported in the company’s consolidated financial statements. Gross Investment: Original price paid for an asset plus capital improvements funded by LTC, without any deductions for depreciation or provision for credit losses. Gross Investment is commonly referred to as undepreciated book value. Independent Living Communities (“ILF”): Seniors housing properties offering a sense of community and numerous levels of service, such as laundry, housekeeping, dining options/meal plans, exercise and wellness programs, transportation, social, cultural and recreational activities, on-site security and emergency response programs. Many offer on-site conveniences like beauty/barber shops, fitness facilities, game rooms, libraries and activity centers. ILFs are also known as retirement communities or seniors apartments. Interest Income: Represents interest income from financing receivables, mortgage loans and other notes. Licensed Beds/Units: The number of beds and/or units that an operator is authorized to operate at seniors housing and long-term care properties. Licensed beds and/or units may differ from the number of beds and/or units in service at any given time. Memory Care Communities (“MC”): Seniors housing properties offering specialized options for seniors with Alzheimer’s disease and other forms of dementia. These facilities offer dedicated care and specialized programming for various conditions relating to memory loss in a secured environment that is typically smaller in scale and more residential in nature than traditional assisted living facilities. These facilities have staff available 24 hours a day to respond to the unique needs of their residents. Metropolitan Statistical Areas (“MSA”): Based on the U.S. Census Bureau, MSA is a geographic entity defined by the Office of Management and Budget (OMB) for use by Federal statistical agencies in collecting, tabulating, and publishing Federal statistics. A metro area contains a core urban area of 50,000 or more population. MSAs 1 to 31 have a population of 19.5M – 2.2M. MSAs 32 to 100 have a population of 2.2M – 0.6M. MSAs greater than 100 have a population of 0.6M – 58K. Cities in a Micro-SA have a population of 264K – 12K. Cities not in a MSA has population of less than 100K. Mezzanine: Mezzanine financing sits between senior debt and common equity in the capital structure, and typically is used to finance development projects, value-add opportunities on existing operational properties, partnership buy-outs and recapitalization of equity. Security for mezzanine loans can include all or a portion of the following credit enhancements; secured second mortgage, pledge of equity interests and personal/corporate guarantees. Mezzanine loans can be recorded for GAAP purposes as either a loan or joint venture depending upon specifics of the loan terms and related credit enhancements. Micropolitan Statistical Areas (“Micro-SA”): Based on the U.S. Census Bureau, Micro-SA is a geographic entity defined by the Office of Management and Budget (OMB) for use by Federal statistical agencies in collecting, tabulating, and publishing Federal statistics. A micro area contains an urban core of at least 10,000 population. GLOSSARY I 28 GLOSSARY |

| 3Q 2025 SUPPLEMENTAL REPORT Mortgage Loan: Mortgage financing is provided on properties based on our established investment underwriting criteria and secured by a first mortgage. Subject to underwriting, additional credit enhancements may be required including, but not limited to, personal/corporate guarantees and debt service reserves. When possible, LTC attempts to negotiate a purchase option to acquire the property at a future time and lease the property back to the borrower. Net Real Estate Assets: Gross real estate investment less accumulated depreciation. Net Real Estate Asset is commonly referred to as Net Book Value (“NBV”). NNN – Triple-net lease which requires the lessee to pay all taxes, insurance, maintenance and repair capital and non-capital expenditures and other costs necessary in the operations of the property. Non-cash Revenue: Straight-line rental income, amortization of lease inducement and effective interest. Non-cash Compensation Charges: Vesting expense relating to restricted stock and performance-based stock units. Normalized EBITDAR Coverage: The trailing twelve month’s earnings from the operator financial statements adjusted for non-recurring, infrequent, or unusual items and before interest, taxes, depreciation, amortization, and rent divided by the operator’s contractual lease rent. Management fees are imputed at 5% of revenues. Normalized EBITDARM Coverage: The trailing twelve month’s earnings from the operator financial statements adjusted for non-recurring, infrequent, or unusual items and before interest, taxes, depreciation, amortization, rent, and management fees divided by the operator’s contractual lease rent. Occupancy: The weighted average percentage of all beds and/or units that are occupied at a given time. The calculation uses the trailing twelve months and is based on licensed beds and/or units which may differ from the number of beds and/or units in service at any given time. Operator Financial Statements: Property level operator financial statements which are unaudited and have not been independently verified by us. Payor Source: LTC revenue by operator underlying payor source for the period presented. LTC is not a Medicaid or a Medicare recipient. Statistics represent LTC's rental revenues times operators' underlying payor source revenue percentage. Underlying payor source revenue percentage is calculated from property level operator financial statements which are unaudited and have not been independently verified by us. Private Pay: Private pay includes private insurance, HMO, VA, and other payors. Purchase Price: Represents the fair value price of an asset that is exchanged in an orderly transaction between market participants at the measurement date. An orderly transaction is a transaction that assumes exposure to the market for a period prior to the measurement date to allow for marketing activities that are usual and customary for transactions involving such assets; it is not a forced transaction (for example, a forced liquidation or distress sale). Real Estate Investments: Represents our investments in real property, financing receivables, mortgage loans receivable and other notes receivables. Rental Income: Represents GAAP rent generated by our owned properties under triple-net leases. RIDEA: Real Estate Investment Trust (REIT) Investment Diversification and Empowerment Act of 2007 Same Property Portfolio (“SPP”): Same property statistics allow for the comparative evaluation of performance across a consistent population of LTC’s leased property portfolio and the Prestige Healthcare mortgage loan portfolio. Our SPP is comprised of stabilized properties occupied and operated throughout the duration of the quarter-over-quarter comparison periods presented (excluding assets sold, assets held-for-sale and SHOP assets). Accordingly, a property must be occupied and stabilized or a minimum of 15 months to be included in our SPP. Each property transitioned to a new operator has been excluded from SPP and will be added back to SPP for the SPP reporting period ending 15 months after the date of the transition. Seniors Housing (“SH”): Consists of independent living, assisted living, and/or memory care properties. Seniors Housing Operating Portfolio (“SHOP”): Includes Seniors Housing properties generally structured to comply with RIDEA. SHOP Net Operating Income (“NOI”): The difference between Resident fees and services and Property operating expense line items on our Consolidated Statements of Income. Skilled Nursing Properties (“SNF”): Seniors housing properties providing restorative, rehabilitative and nursing care for people not requiring the more extensive and sophisticated treatment available at acute care hospitals. Many SNFs provide ancillary services that include occupational, speech, physical, respiratory and IV therapies, as well as sub-acute care services which are paid either by the patient, the patient’s family, private health insurance, or through the federal Medicare or state Medicaid programs. Stabilized: Properties are generally considered stabilized upon the earlier of achieving certain occupancy thresholds (e.g. 80% for SNFs and 90% for ALFs) and, as applicable, 12 months from the date of acquisition/lease transition/restructure or, in the event of a de novo development, redevelopment, major renovations or addition, 24 months from the date the property is first placed in or returned to service, or properties acquired in lease-up. Trailing Twelve Months NOI: For the owned portfolio under triple-net leases, rental income excluding real estate tax reimbursement, straight-line rent write-off and rental income from properties sold during the trailing twelve months. For the owned portfolio under our SHOP segment, represents SHOP NOI during the trailing twelve months. For owned properties accounted for as financing receivables, mortgage loan receivables and notes receivables, NOI includes cash interest income and effective interest during the trailing twelve months and excludes loan payoffs during the trailing twelve months. For Unconsolidated JV, NOI includes income from our investments in joint ventures during the trailing twelve months. Under Development Properties (“UDP”): Development projects to construct seniors housing properties. GLOSSARY I 29 GLOSSARY |

| 3Q 2025 SUPPLEMENTAL REPORT FORWARD-LOOKING STATEMENTS This supplemental information contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, adopted pursuant to the Private Securities Litigation Reform Act of 1995. Statements that are not purely historical may be forward-looking. You can identify some of the forward-looking statements by their use of forward-looking words, such as ‘‘believes,’’ ‘‘expects,’’ ‘‘may,’’ ‘‘will,’’ ‘‘should,’’ ‘‘seeks,’’ ‘‘approximately,’’ ‘‘intends,’’ ‘‘plans,’’ ‘‘estimates’’ or ‘‘anticipates,’’ or the negative of those words or similar words. Examples of forward-looking statements include the Company’s 2025 full-year guidance and statements regarding the Company’s SHOP pipeline, anticipated growth, and future strategy. Forward- looking statements involve inherent risks and uncertainties regarding events, conditions and financial trends that may affect our future plans of operation, business strategy, results of operations and financial position. A number of important factors could cause actual results to differ materially from those included within or contemplated by such forward-looking statements, including, but not limited to, our dependence on our operators for revenue and cash flow; government regulation of the health care industry; changes in federal, state, or local laws limiting REIT investments in the health care sector; federal and state health care cost containment measures including reductions in reimbursement from third-party payors such as Medicare and Medicaid; required regulatory approvals for operation of health care facilities; a failure to comply with federal, state, or local regulations for the operation of health care facilities; the adequacy of insurance coverage maintained by our operators; our reliance on a few major operators; our ability to renew leases or enter into favorable terms of renewals or new leases; the impact of inflation, operator financial or legal difficulties; the sufficiency of collateral securing mortgage loans; an impairment of our real estate investments; the relative illiquidity of our real estate investments; our ability to develop and complete construction projects; our ability to invest cash proceeds for health care properties; a failure to qualify as a REIT; our ability to grow if access to capital is limited; and a failure to maintain or increase our dividend. For a discussion of these and other factors that could cause actual results to differ from those contemplated in the forward-looking statements, please see the discussion under ‘‘Risk Factors’’ and other information contained in our Annual Report on Form 10-K for the fiscal year ended December 31, 2024 and in our publicly available filings with the Securities and Exchange Commission. We do not undertake any responsibility to update or revise any of these factors or to announce publicly any revisions to forward-looking statements, whether as a result of new information, future events or otherwise. Although our management believes that the assumptions and expectations reflected in such forward-looking statements are reasonable, no assurance can be given that such expectations will prove to have been correct. The actual results achieved may differ materially from any forward-looking statements due to the risks and uncertainties of such statements. 30 Founded in 1992, LTC Properties, Inc. (NYSE: LTC) is a self-administered real estate investment trust (REIT) investing in seniors housing and health care properties primarily through RIDEA, triple-net leases, joint ventures and structured finance solutions including preferred equity and mezzanine lending. LTC’s portfolio encompasses Skilled Nursing Facilities (SNF) and Seniors Housing (SH) consisting of Assisted Living Communities (ALF), Independent Living Communities (ILF), Memory Care Communities (MC) and combinations thereof. Our main objective is to build and grow a diversified portfolio that creates and sustains shareholder value while providing our stockholders current distribution income. To meet this objective, we seek properties operated by regional operators, ideally offering upside and portfolio diversification (geographic, operator, property type and investment vehicle). For more information, visit www.LTCreit.com. FORWARD-LOOKING STATEMENTS AND NON-GAAP INFORMATION NON-GAAP INFORMATION This supplemental information contains certain non-GAAP information including EBITDAre, adjusted EBITDAre, FFO, FFO excluding non-recurring items, FAD, FAD excluding non-recurring items, adjusted interest coverage ratio, and adjusted fixed charges coverage ratio. A reconciliation of this non-GAAP information is provided on pages 21, 25, 26 and 27 of this supplemental information, and additional information is available under the “Non-GAAP Financial Measures” subsection under the “Filings” section of our website at www.LTCreit.com. |